Navigating the world of commercial trucking insurance can feel like driving through a dense fog. Quotes vary wildly, and understanding what you’re actually paying for is crucial for protecting your business and your bottom line. If you’re searching for the “average insurance cost for semi trucks,” you’ve likely discovered there’s no single, simple number. That’s because insurance isn’t a commodity; it’s a tailored assessment of risk.

This guide will cut through the complexity. We’ll provide you with realistic price frameworks, break down the factors that determine your premium, and offer actionable strategies to manage your insurance expenses effectively. Whether you’re an owner-operator just starting out or a fleet manager reviewing policies, this article is your roadmap to making informed, confident decisions about your semi-truck insurance.

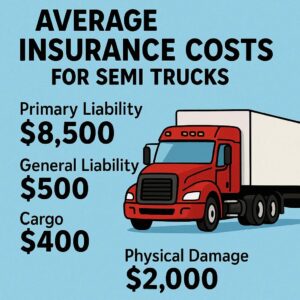

Average Insurance Costs for Semi Trucks

What Exactly Are You Insuring? Breaking Down Coverage Types

Before we talk numbers, it’s vital to understand what goes into a policy. A semi-truck insurance policy is typically a package of several core coverages, each with its own cost.

Primary Liability Insurance

This is the foundational and legally required coverage in most states. It covers bodily injury and property damage to others if you are at fault in an accident. It does not cover damage to your own truck or your injuries.

Industry Insight: “Primary liability is your financial responsibility on the road. It’s non-negotiable and forms the base of any commercial auto policy,” notes a veteran insurance underwriter.

Physical Damage Coverage

Often called “collision and comprehensive,” this protects your truck and trailer.

-

Collision: Covers damage from an accident with another vehicle or object.

-

Comprehensive: Covers non-collision events like theft, fire, vandalism, or hitting an animal.

Cargo Insurance

This protects the goods you are hauling. Shippers often require specific cargo liability limits. The value and type of cargo (e.g., general freight vs. hazardous materials) dramatically affect this premium.

Motor Truck Cargo Legal Liability

This is a crucial distinction. It covers your legal liability for the cargo if it’s damaged due to your negligence (e.g., a wreck caused by you). All-risk cargo insurance is broader but more expensive.

Uninsured/Underinsured Motorist Coverage

Protects you and your assets if you’re hit by a driver with little or no insurance.

Realistic Cost Ranges: What Can You Actually Expect?

Now for the figures. Remember, these are national averages and starting points. Your specific quote will differ based on the factors we detail in the next section.

Important Note: Insurance premiums are typically quoted as an annual cost, though many businesses pay monthly. All figures below are annual estimates.

Average Cost Table for Owner-Operators (1 Truck)

| Coverage Type | Low-End Annual Estimate | High-End Annual Estimate | Key Influencing Factors |

|---|---|---|---|

| Primary Liability Only | $8,000 – $12,000 | $15,000 – $25,000+ | Driving record, state, radius of operation. |

| Liability + Physical Damage | $12,000 – $18,000 | $25,000 – $40,000+ | Truck value, deductible choice, driving record. |

| Full Package (Lia. + P.D. + Cargo) | $15,000 – $25,000 | $40,000 – $70,000+ | All factors combined, especially cargo type. |

Cost Breakdown for Small Fleets (3-5 Trucks)

Fleets often see a per-unit cost reduction due to volume, but total outlay is higher.

-

Per Truck Average: $10,000 – $20,000 annually for a robust package.

-

Total Fleet Cost: $30,000 – $100,000+ annually.

Critical Reminder: A new authority (MC/DOT number) will always pay more—often 30-50% more—than an established operation with several years of proven safety history. This is a major initial cost of doing business.

The 7 Key Factors That Determine Your Premium

Insurance companies are in the business of assessing risk. Your premium is their price for assuming your specific risk profile. Here’s what they scrutinize.

1. Driver & Operational History

This is the most significant factor.

-

Driving Record (MVR): Clean records save money. Violations, especially serious ones (DUIs, reckless driving), and at-fault accidents spike premiums.

-

Experience: Drivers with less than 2-3 years of verifiable CDL experience cost more to insure.

-

CSA Scores: Your FMCSA Compliance, Safety, Accountability scores are a public report card. High scores in Unsafe Driving or Crash Indicator categories lead to higher premiums.

2. Type of Operation & Radius

-

Radius: Local/regional operations typically cost less than long-haul (national) due to less time on the road and familiarity with routes.

-

Freight Type: Hauling general dry van freight is standard risk. Specialized operations like flatbed, reefer, auto transport, or—most notably—hazardous materials carry significantly higher liability and cost.

3. Truck & Equipment Details

-

Vehicle Value: A brand-new $180,000 Peterbilt costs much more to insure for physical damage than a paid-off 2015 model.

-

Safety Technology: Discounts are increasingly available for trucks equipped with approved telematics (ELDs), dash cams, collision mitigation systems, and lane departure warnings.

4. Cargo Value & Liability

-

High-Value Cargo: Electronics, pharmaceuticals, and high-end clothing require higher cargo limits, increasing cost.

-

Sensitive Cargo: Temperature-controlled (reefer) or fragile goods present a greater risk of financial loss.

5. Deductible Choices

The amount you pay out-of-pocket on a claim directly impacts your premium.

-

High Deductible (e.g., $5,000) = Lower Annual Premium.

-

Low Deductible (e.g., $1,000) = Higher Annual Premium.

Choose a deductible your business can comfortably absorb in an emergency.

6. Coverage Limits

Higher limits mean higher premiums, but also greater protection. Carrying only the minimum legal liability ($750,000) is cheaper but may be insufficient in a catastrophic accident. Many shippers require $1 million+ in liability.

7. Business History & Credit

-

Years in Business: New authorities are the highest risk.

-

Business Financials/Credit: Insurers may see a correlation between financial stability and claim risk.

Actionable Strategies to Lower Your Insurance Costs

You are not powerless against premium costs. Proactive management can yield substantial savings.

1. Prioritize Safety Above All Else

-

Implement a formal driver safety program.

-

Regularly review CSA scores and address violations immediately.

-

Use pre-employment screening services (PSP reports) to hire responsibly.

2. Leverage Technology for Discounts

-

Install insurer-approved telematics/gps tracking and dash cams (especially facing forward and the driver). These devices exonerate good drivers and provide data for coaching.

-

Invest in collision mitigation systems (e.g., Bendix Wingman, Meritor WABCO).

3. Optimize Your Policy Structure

-

Bundle Coverages with one insurer.

-

Adjust Deductibles to a level that makes sense for your cash flow.

-

Annually Review Limits and Values to avoid over-insuring old equipment.

4. Build and Maintain Your Profile

-

Stay in business and operate cleanly. Each year of safe operation builds credibility.

-

Develop a strong relationship with a specialized commercial trucking insurance agent or broker. Their expertise and market access are invaluable.

5. Consider Alternative Risk Options (For Larger Fleets)

-

High Deductible Plans: For fleets with strong safety records and financial reserves.

-

Captive Insurance: A form of self-insurance for very large, stable operations.

Helpful Checklist for Getting an Accurate Quote

When you’re ready to shop for insurance, have this information ready:

-

Complete list of drivers with full names, dates of birth, CDL numbers, and 3-5 years of experience history.

-

Motor Vehicle Reports (MVRs) for all drivers.

-

Your MC/DOT number and current CSA score snapshot.

-

Detailed information on all vehicles: Year, make, model, VIN, purchase price/current value.

-

Description of operations: Radius, percentage of freight type (e.g., 80% dry van, 20% flatbed).

-

Desired coverage limits and deductibles.

-

Your loss history (previous claims) for the last 5 years.

Conclusion

The average insurance cost for a semi truck is a dynamic figure, deeply personal to your business’s risk profile, ranging from foundational liability at around $10,000 to comprehensive packages exceeding $40,000 annually. By understanding the core coverages, meticulously managing the seven key rating factors, and proactively implementing safety and technology strategies, you can transform insurance from a daunting cost into a manageable, strategic investment in your operation’s longevity and security.

Frequently Asked Questions (FAQ)

Q: What is the cheapest semi-truck insurance I can get?

A: The absolute cheapest would be bare-minimum liability coverage for an experienced driver with a perfect record hauling low-risk freight in a regional area with an older truck. However, “cheapest” often means least protection. Adequate coverage is more important than the lowest price.

Q: How much should I budget for insurance as a new owner-operator?

A: New authorities should budget aggressively. For a full package (liability, physical damage, cargo), realistically budget $20,000 to $35,000 for your first year. This cost should decrease significantly with 2-3 years of clean operation.

Q: Does my personal auto insurance cover me when driving my semi?

A: Absolutely not. Your personal auto policy explicitly excludes coverage for vehicles used in a commercial business. You must have a separate, active commercial auto policy.

Q: How often should I shop for new insurance quotes?

A: It’s prudent to review your policy and get comparative quotes annually, about 60 days before your renewal date. Avoid switching insurers mid-term unless necessary, as cancellation fees may apply.

Q: Can I pay my premium monthly?

A: Most insurers offer monthly payment plans, but they often include installment fees (e.g., $5-$15 per payment). Paying the annual premium in full usually avoids these fees.