Buying a home in Illinois is an exciting journey, but it comes with a stack of paperwork and a list of closing costs that can be confusing. One line item that often raises questions is title insurance. Unlike other recurring insurance premiums, you pay for title insurance once at closing, and it provides a lifetime of protection. But what exactly are you paying for, and how is the title insurance cost in Illinois determined? This comprehensive guide will break down everything you need to know, from the basics of what title insurance is to the specific factors that influence its price in the Prairie State.

Our goal is to demystify this essential part of the home-buying process. We’ll provide you with clear, actionable information so you can approach your closing table with confidence, understanding the value and the cost of this critical protection.

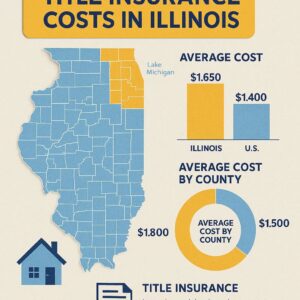

Title Insurance Cost in Illinois

What is Title Insurance and Why is it Required in Illinois?

Before we dive into costs, let’s clarify what we’re talking about. Title insurance is a unique form of indemnity insurance that protects real estate owners and lenders against financial loss from defects in a property’s title.

Think of a property’s “title” as its legal history and chain of ownership. A “clean” title means there are no outstanding legal claims or disputes. However, hidden issues can lurk in the past: old unpaid liens, forged signatures on previous deeds, undisclosed heirs, recording errors, or even simple mistakes in the public record. These are called “title defects.”

Why it’s essential: A standard property search might miss these hidden problems. If a defect emerges after you purchase the home, you could face expensive legal battles or even lose your ownership claim. Title insurance shields you from this risk.

In Illinois, while a lender’s policy (which protects the bank’s investment) is almost universally required to secure a mortgage, an owner’s policy (which protects your equity) is optional but highly recommended. It’s a one-time premium for peace of mind that lasts as long as you or your heirs own the property.

How is Title Insurance Cost Calculated in Illinois?

Illinois is a “promulgated rate” state for title insurance. This means the Illinois Department of Financial and Professional Regulation (IDFPR) reviews and approves the premium rates. All title insurance companies in the state must charge these same base rates. You won’t find wildly different base premiums from one company to another.

The primary factor determining your premium is the purchase price or loan amount of the property. The cost is not a flat percentage but uses a sliding scale, where the rate per thousand dollars decreases as the property value increases.

Illinois Title Insurance Rate Schedule (Simplified Example)

Note: The following is a simplified illustration based on common Illinois rate structures. Exact rates are filed with the IDFPR.

| Policy Coverage Amount | Approximate Owner’s Policy Premium | Approximate Lender’s Policy (ALTA) Premium |

|---|---|---|

| $100,000 | $850 | $575 |

| $250,000 | $1,325 | $925 |

| $500,000 | $1,925 | $1,325 |

| $750,000 | $2,400 | $1,650 |

| $1,000,000 | $2,875 | $1,975 |

Important Note: The lender’s policy (often called an ALTA policy) is typically less expensive than the owner’s policy. When purchased simultaneously in a standard transaction, most companies offer a significant “simultaneous issue” discount on the lender’s policy. The table above reflects common discounted lender’s policy rates when issued with an owner’s policy.

Breakdown of a Typical Title Insurance Bill in Illinois

Your settlement statement (the HUD-1 or Closing Disclosure) will list several charges related to title services. It’s crucial to understand that the “title insurance cost” is more than just the state-regulated premium.

Here’s what you might see:

-

Title Insurance Premium (Owner’s Policy): The state-regulated fee for your owner’s title insurance policy, based on the sales price.

-

Title Insurance Premium (Lender’s Policy): The state-regulated fee for the lender’s policy, based on the loan amount, often issued at a simultaneous rate.

-

Title Search & Examination Fee: This is the charge for the labor-intensive work of digging through public records to create the title history report and identify any potential issues. This fee is negotiable and can vary between title companies.

-

Closing/Escrow/Settlement Fee: This covers the administrative cost of handling the closing, preparing documents, and disbursing funds.

-

Endorsements: These are add-ons to the standard policy that cover specific risks. Common ones in Illinois include:

-

Condominium Endorsement

-

Planned Unit Development (PUD) Endorsement

-

Survey Endorsement (requires an up-to-date survey)

-

A key point from industry experts: “Many homebuyers focus solely on the state-set premium, but the ancillary fees for the search, examination, and closing services are where shopping can lead to real savings. Always ask for a detailed fee breakdown from any title company you consider.” – Chicago Area Title Agent

Key Factors That Influence Your Final Cost

While the base premium is fixed, your final total cost can be influenced by several variables:

-

Property Value: The single biggest determinant of the premium.

-

Loan Amount: Directly sets the cost for the lender’s policy.

-

Property Type & History: A newly built home on subdivided land or a centuries-old property in Chicago with a complex history will require a more extensive (and potentially more expensive) title search.

-

Choice of Title Company/Agent: Their fees for search, examination, and closing services can differ.

-

Negotiation: In Illinois, it is customary for the seller to pay for the owner’s title insurance policy. The buyer typically pays for the lender’s policy and the title search/related fees. However, this is a point of negotiation in the purchase contract.

-

Refinancing: If you are refinancing your mortgage, you will not need a new owner’s policy (yours is still valid), but your new lender will require a fresh lender’s policy. This is called a “re-issue rate” or “refinance rate,” which is substantially lower than a standard lender’s policy premium—often 40-50% off—if you can provide a copy of your previous owner’s policy.

How to Potentially Save on Title Insurance in Illinois

-

Shop for Title Services: You have the right to choose your title company. Get quotes from 2-3 companies. Compare their fees for the title search, examination, and settlement services—not just the regulated premium.

-

Ask About Re-Issue Rates: If you are refinancing, proactively provide a copy of your existing owner’s policy to the title company to qualify for the lower re-issue rate on the new lender’s policy.

-

Negotiate with the Seller: While custom dictates who pays what, everything is negotiable in a real estate contract. In a buyer’s market, you may be able to ask the seller to cover more of the title-related costs.

-

Bundle Services: Some companies offer slight discounts if you also use them for other services like real estate attorney review (common in Illinois) or escrow.

-

Ask About Package Deals: Some title agents may offer a “package” price for all their services (search, exam, closing, insurance).

Title Insurance for Refinancing vs. Purchasing: A Cost Comparison

The cost structure is fundamentally different.

| Aspect | Purchase Transaction | Refinance Transaction |

|---|---|---|

| Owner’s Policy | New policy purchased. Typically paid by seller. | Not required. Your original policy remains in effect. |

| Lender’s Policy | New policy required. Paid by buyer at simultaneous issue rate. | New policy required. Paid by homeowner, but often at a lower re-issue rate. |

| Primary Cost Driver | Purchase price of the home. | Loan amount of the new mortgage. |

| Typical Total Cost | Higher, due to the need for a full owner’s policy. | Lower, as you are only purchasing a lender’s policy at a discounted rate. |

Common Misconceptions About Title Insurance Costs

-

Myth: “Shopping around doesn’t matter since rates are state-set.” Reality: While the insurance premium is fixed, the service fees (search, exam, closing) are not and can vary by hundreds of dollars.

-

Myth: “I don’t need an owner’s policy if I have a lender’s policy.” Reality: The lender’s policy only protects the bank’s financial interest. It does not protect your down payment or your home’s equity.

-

Myth: “Title insurance is an unnecessary closing cost.” Reality: It is one of the most important protections you buy, guarding against potentially catastrophic, hidden title defects.

The Closing Process: What to Expect with Title in Illinois

The title company plays a central role in your closing:

-

Opening the Order: Once you have a signed contract, a title agent begins the search and examination.

-

Clearing Title Issues: Any problems (like an old lien) must be resolved (or “cured”) before closing. The seller is usually responsible for this.

-

Preparing for Closing: The agent prepares the title commitment (a promise to insure) and all closing documents.

-

The Closing Meeting: You sign the final paperwork, funds are transferred, and the deed is recorded with the county.

-

Policy Issuance: After recording, the final title insurance policy is prepared and mailed to you. Keep this document in a safe, permanent place.

Conclusion

Understanding title insurance cost in Illinois involves looking beyond a single number. It’s a combination of a state-regulated premium based on your home’s value and negotiable fees for vital services that ensure your ownership is sound. By knowing how costs are structured, what factors influence them, and where you can shop for value, you can make informed decisions that protect your investment without overpaying. Remember, this one-time fee provides a lifetime of defense against the unpredictable—making it a cornerstone of a secure real estate transaction.

Frequently Asked Questions (FAQ)

Q: Who typically pays for title insurance in Illinois?

A: Customarily, the seller pays for the owner’s title insurance policy, and the buyer pays for the lender’s policy and the title search/examination fees. This is always a point of negotiation in the real estate contract.

Q: Is title insurance mandatory in Illinois?

A: An owner’s policy is not legally mandatory but is strongly advised. A lender’s policy is almost always required by the mortgage company to protect their loan.

Q: How much is title insurance on a $300,000 house in Illinois?

A: For a $300,000 purchase, the owner’s title insurance premium would be approximately $1,500 (based on state rates). The simultaneous-issue lender’s policy would be approximately $1,050. Additional fees for search, exam, and closing would apply.

Q: Can I shop for my own title company in Illinois?

A: Yes, you have the right to select the title company. Your real estate agent or lender may recommend one, but you are free to choose your own.

Q: Do I need a new title insurance policy when I refinance?

A: No. Your existing owner’s policy remains valid. However, your new lender will require a new lender’s policy. Be sure to ask for a “re-issue rate” discount by providing your old policy.