Buying a home in Massachusetts is an exciting journey, but it comes with a labyrinth of paperwork and important financial decisions. One item on your closing cost worksheet that often prompts questions is title insurance. Unlike ongoing insurance policies, title insurance is a one-time premium paid at closing that protects your most valuable asset from hidden risks in its history. Understanding title insurance cost in Massachusetts is crucial for any savvy homebuyer or homeowner looking to refinance. This comprehensive guide will demystify the fees, explain what you’re paying for, and help you navigate this essential piece of the real estate transaction.

Title Insurance Cost in Massachusetts

What is Title Insurance and Why is it Required?

Before we dive into costs, let’s clarify what title insurance actually does. When you purchase a home, you’re buying the “title” or legal rights to that property. The property’s history, or “chain of title,” can sometimes contain hidden defects like unpaid taxes, forged signatures on old deeds, undisclosed heirs, or clerical errors. These issues can threaten your legal ownership.

Title insurance is a safeguard. It protects homeowners and lenders from financial loss due to such defects in the title. There are two primary policies:

-

Lender’s Title Insurance (Loan Policy): This is almost always required by your mortgage company. It protects the lender’s financial interest in the property up to the loan amount. It does not protect you, the homeowner.

-

Owner’s Title Insurance (Owner’s Policy): This is optional but highly recommended. It protects your equity and legal right to the property for as long as you or your heirs own it. It is a one-time premium paid at closing.

As noted by real estate attorney Jane Mitchell, “Title insurance is the shield that protects your castle from claims rooted in the past. It’s not an inspection of the future, but a guarantee against the ghosts in the property’s paperwork.”

Breaking Down the Cost of Title Insurance in Massachusetts

The total title insurance cost in Massachusetts is not a single flat fee. It’s comprised of the insurance premium itself (regulated by the state) and associated services provided by the title company or attorney.

1. The Regulated Insurance Premium

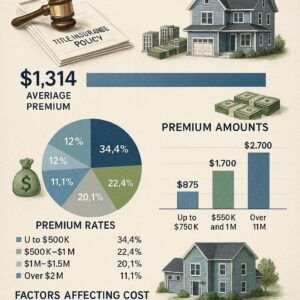

Massachusetts is a “promulgated rate” state. This means the Commonwealth’s Division of Insurance sets the rates for title insurance premiums. Companies cannot compete on price for the pure insurance premium, ensuring consistency. The premium is based on the purchase price or loan amount.

Owner’s Title Insurance Premium Calculator (Sample):

| Purchase Price of Home | Estimated Owner’s Policy Premium (Rate) |

|---|---|

| $500,000 | $1,375.00 |

| $750,000 | $1,925.00 |

| $1,000,000 | $2,375.00 |

| $1,500,000 | $3,175.00 |

Note: These are illustrative samples based on the promulgated rate structure. Your exact premium will be calculated by your title agent.

Lender’s Policy Premium: This is typically lower than the owner’s policy. In many cases, if you purchase an owner’s policy simultaneously with a lender’s policy, you qualify for a “simultaneous issue rate” or reissue rate, which is a significant discount on the lender’s portion.

2. Title Search and Examination Fees

This is the labor-intensive work behind the policy. A title professional will search public records at the county registry of deeds and other offices to uncover any issues with the title. This fee is separate from the insurance premium and can vary between companies.

3. Settlement/Closing Fee

This fee covers the coordination and execution of the closing, including document preparation, notary services, and disbursement of funds.

4. Endorsements

These are add-ons to the standard policy that cover specific situations, such as properties in a homeowners association (HOA) or with specific easements. Each endorsement adds a small fee.

Who Pays for Title Insurance in Massachusetts?

This is a common point of negotiation, governed by local custom and the purchase and sale agreement.

-

Traditional Custom: In much of Massachusetts, especially eastern counties, the seller customarily pays for the owner’s title insurance policy. The buyer typically pays for the lender’s title insurance policy.

-

Negotiation: This is not a law, but a strong custom. The responsibility for paying these costs can be negotiated between buyer and seller during the offer process. Always clarify this in your contract.

-

Refinancing: When you refinance your mortgage, you are required to purchase a new lender’s title insurance policy. You do not need a new owner’s policy, as your original policy remains in effect for as long as you own the home.

Important Note for Readers: “Don’t let local custom be a surprise. On your very first offer, have your real estate agent explicitly outline who is expected to pay for the owner’s and lender’s title policies based on the property location. This should be a clear line item in your estimated closing costs.”

Factors That Influence Your Total Title Service Cost

While the insurance premium itself is fixed, the total cost for title services can vary. Here’s what affects the bottom line:

-

Property Value: The single biggest factor for the premium.

-

Loan Amount: Directly impacts the lender’s policy cost.

-

Property History: A complex history with multiple past owners, trusts, or old subdivisions may require a more extensive (and thus more expensive) title search.

-

Geographic Location: Title search and settlement fees may differ between the Berkshires, Boston, and Cape Cod.

-

Title Company or Attorney Choice: You have the right to shop for title services. While the premium is fixed, their fees for search, examination, and closing can be compared.

How to Get the Best Value on Title Insurance

-

Shop Around: Obtain quotes from 2-3 reputable title companies or real estate attorneys. Compare their service fees, not the regulated premium.

-

Ask About Bundling: Always inquire about the “simultaneous issue rate” discount when getting both an owner’s and a lender’s policy.

-

Request a Reissue Rate: If the property was sold or refinanced recently, ask if the title company can offer a reissue rate, which can save you up to 30-40% on the premium.

-

Read Reviews: Look for companies with a reputation for accuracy, responsiveness, and clear communication. A smooth closing is valuable.

-

Understand the Quote: Request a detailed, line-item breakdown of all charges (the Closing Disclosure, or CD, will have this later). Know what each fee represents.

Comparative Table: Owner’s vs. Lender’s Title Insurance

| Feature | Owner’s Title Insurance Policy | Lender’s Title Insurance Policy |

|---|---|---|

| Who It Protects | The homeowner and their heirs. | The mortgage lender. |

| Coverage Duration | For as long as you or your heirs own the property. | Until the mortgage is paid off or refinanced. |

| Cost Basis | Based on the full purchase price of the home. | Based on the loan amount. |

| Mandatory? | Optional, but highly advisable. | Almost always required by the lender. |

| Who Usually Pays | Often the seller (by custom in MA). | Usually the buyer. |

Conclusion

Navigating the title insurance cost in Massachusetts is a key step in a secure real estate transaction. The cost is a one-time investment that provides lasting peace of mind, protecting your property rights from unforeseen claims. Remember that while the insurance premium itself is state-regulated, you can shop for competitive fees on title services. By understanding the components, who typically pays, and asking the right questions, you can ensure you’re getting essential protection and the best possible value for this critical part of your home investment.

Frequently Asked Questions (FAQ)

Q: Is owner’s title insurance really worth it in Massachusetts?

A: Absolutely. Given the state’s long history and complex property records, hidden title defects are a real possibility. The one-time premium protects your financial investment for decades, often for less than the cost of a single monthly mortgage payment.

Q: Can I skip title insurance if I pay cash for a home?

A: While not legally required for a cash purchase, it is arguably even more critical. Without a lender requiring it, you have no protection against title defects. You are solely responsible for any legal challenges or financial losses.

Q: How much should I budget for total title-related closing costs?

A: As a rough estimate, budget between 0.5% and 1% of the purchase price for all title-related costs (insurance premiums, search, settlement). For a $750,000 home, this could range from $3,750 to $7,500.

Q: Does my homeowner’s insurance policy cover title issues?

A: No. Standard homeowner’s insurance covers physical damage to the structure and liability. It does not protect against legal ownership claims, which is the exclusive domain of title insurance.

Additional Resources

-

For official information and resources on insurance in the state, visit the Massachusetts Division of Insurance website: https://www.mass.gov/orgs/division-of-insurance

-

The American Land Title Association (ALTA) provides extensive consumer guides on title insurance: https://www.alta.org/consumers/