Let’s be honest: figuring out the cost of dental insurance can feel a bit like deciphering a foreign language. You see numbers thrown around—$20 a month, $50 a month, “100% coverage”—but what does it actually mean for your wallet? If you’ve been putting off a trip to the dentist because you’re worried about the bill, or you’re simply trying to budget for the year ahead, you’ve come to the right place.

Welcome to your friendly, no-nonsense guide to understanding the dental insurance average cost. We’re going to peel back the layers, look at the real numbers, and help you figure out what kind of coverage makes sense for you. Think of this as a chat over coffee, where we make sense of the fine print together.

We won’t just throw a single number at you, because the truth is, the cost isn’t one-size-fits-all. It depends on where you get your insurance, the type of plan you choose, and even the kind of dental care you anticipate needing.

So, grab a cup of coffee, get comfortable, and let’s dive into the details of dental insurance pricing.

What You Will Discover in This Guide

-

The honest breakdown of what “average” really means for monthly premiums.

-

A clear comparison of the main types of dental plans and their price tags.

-

The hidden costs: deductibles, copays, and coinsurance explained.

-

How to match a plan to your life, whether you’re an individual, a family, or a senior.

-

Practical tips for saving money, both on your premiums and at the dentist’s office.

Let’s get started on the path to a healthy smile without the financial stress.

The Real Numbers: Breaking Down the Average Monthly Premium

When people search for “dental insurance average cost,” they usually want a bottom-line number. What will this actually cost me every month? It’s a fair question. While prices vary by location and provider, we can establish a realistic range based on industry standards.

For most Americans, dental insurance is obtained through an employer. In these cases, the employer often covers a significant portion of the premium, making it highly affordable for the employee. However, if you are shopping for an individual or family plan on the private market, you are responsible for the full cost.

Here is the realistic breakdown of what you can expect to pay per month:

-

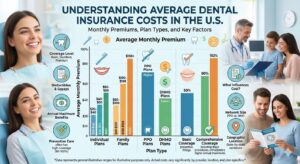

Individual Plans: On average, you can expect to pay between $20 and $60 per month.

-

Family Plans: For coverage that includes a spouse and children, the average monthly cost typically ranges from $50 to $150 per month.

Important Note: These are averages. A basic, preventative-only plan in a rural area might be as low as $15 per month. A comprehensive plan with a high annual maximum in a major city could easily exceed $70 for an individual.

Think of your monthly premium as a membership fee. It’s the cost you pay to be in the insurance network, regardless of whether you actually visit the dentist that month. It keeps your coverage active and ensures that when you do need care, the insurance company will help pay for it.

The “Unlock” Fees: Deductibles and Annual Maximums

Your monthly premium isn’t the only number you need to look at. To truly understand the cost of dental insurance, you have to look at the other key financial components: the deductible and the annual maximum. These two factors dictate when the insurance starts paying and how much they will pay in a year.

Understanding Your Deductible

A deductible is the amount you have to pay out-of-pocket for certain services before your insurance company starts to chip in. Think of it as unlocking your benefits for the year.

-

The Average Cost: For most individual dental plans, the deductible ranges from $50 to $100 per person.

-

How it Works: Let’s say you have a $50 deductible and need a filling that costs $150. You will pay the first $50 (your deductible), and then the insurance will cover their portion of the remaining $100, based on your plan’s coinsurance.

-

Family Deductibles: Family plans usually have an aggregate deductible, meaning once a certain total amount is paid for all family members, the coverage kicks in for everyone. This is often two to three times the individual deductible.

-

Preventative Care Exception: Here’s a crucial piece of good news: almost all plans waive the deductible for preventative care. This means your cleanings and checkups are covered from day one, encouraging you to maintain your oral health without having to meet your deductible first.

The Coverage Cap: Annual Maximum

The annual maximum is the total amount of money your insurance company will pay toward your dental care in one calendar year. After you hit this limit, you are responsible for 100% of the costs until the plan resets the next year.

-

The Average Cost (Limit): The vast majority of dental insurance plans have an annual maximum that falls between $1,000 and $2,000 per person.

-

Why It Matters: This is a critical number. Major dental work, like a crown, can easily cost over $1,000. If you need two crowns in a year, you will likely blow past your $1,500 maximum and have to pay for the second one entirely on your own.

-

Inflation and History: It’s worth noting that these annual maximums have remained relatively stagnant for decades, while the cost of dental procedures has risen with inflation. This is a key reason why having insurance is a great help, but it rarely covers 100% of very extensive dental work.

Decoding the Coverage: 100/80/50 and Other Formulas

You’ll often see dental plans described with a series of numbers, like “100-80-50.” This shorthand is actually a simple way to explain how the plan pays for different categories of care. This is known as coinsurance—your share of the costs after you’ve met your deductible.

Once you’ve paid your deductible, the insurance company pays a percentage of the bill, and you pay the rest. Here’s what those numbers typically mean:

1. Preventative Care (The 100%)

This is the foundation of most plans.

-

What it is: Routine exams, regular cleanings (usually twice a year), and routine x-rays.

-

Average Coverage: Plans almost always cover 100% of these costs. This is why it’s often said that dental insurance pays for itself if you go for your regular checkups. You pay the premium, and in return, you get two fully covered cleanings, which can cost over $200 each if paid out-of-pocket.

2. Basic Restorative Care (The 80%)

This category covers common dental problems.

-

What it is: Fillings, simple extractions, and sometimes root canals and periodontal (gum) therapy.

-

Average Coverage: Plans typically cover about 80% of these costs, leaving you responsible for the other 20%.

-

Example: If a filling costs $200, your insurance would pay $160, and you would pay a $40 copay (assuming your deductible is met).

3. Major Restorative Care (The 50%)

This is the most expensive category of care.

-

What it is: Crowns, bridges, dentures, inlays, onlays, and complex oral surgery.

-

Average Coverage: Here, the insurance company usually picks up 50% of the tab, and you pay the other 50%.

-

Example: If a crown costs $1,200, you and your insurance would each pay $600. Remember, this payment counts toward your annual maximum.

Reader’s Tip: Always look at the “major care” coinsurance and your annual maximum together. A 50% coinsurance on a $2,000 crown means you pay $1,000, which could quickly use up a large chunk of a $1,500 annual maximum if you have other work done that year.

Comparing Your Options: PPO, HMO, and Indemnity Plans

The type of plan you choose has a massive impact on the dental insurance average cost and how you receive care. Here are the three most common structures you’ll encounter.

Dental PPO (Preferred Provider Organization)

This is the most popular type of dental plan in the U.S.

-

How it works: You choose a primary dentist from the insurance company’s network of “preferred” providers who have agreed to offer services at a discounted rate.

-

The Cost: PPOs generally have higher monthly premiums than HMOs but offer more flexibility. You can see an out-of-network dentist, but it will cost you more.

-

Pros: Good balance of cost and flexibility, large networks, no need for referrals.

-

Cons: You may have to switch dentists if your current one isn’t in the network.

Dental HMO (Health Maintenance Organization)

Sometimes called “DHMO” or “capitation” plans, these are often the most budget-friendly option for monthly premiums.

-

How it works: You must choose a primary care dentist from a specific network. This dentist manages all your care. There is typically no deductible and fixed copays for services.

-

The Cost: Monthly premiums are significantly lower than PPOs—sometimes as low as $10-$15 per month. However, you have the least flexibility.

-

Pros: Lowest monthly cost, predictable copays, no annual maximums.

-

Cons: You must stay in-network, you need a referral to see a specialist, and you have less choice in providers.

Dental Indemnity Plans (Fee-for-Service)

These are the traditional insurance plans, offering the most freedom but often at a higher cost.

-

How it works: You can go to any dentist you like. You pay for the service upfront, and then the insurance company reimburses you for a set percentage of the cost.

-

The Cost: Premiums tend to be the highest. You also have to deal with paperwork and waiting for reimbursement checks.

-

Pros: Complete freedom to choose any dentist.

-

Cons: Highest premiums, potential for higher out-of-pocket costs, and more administrative work.

Quick Comparison: Plan Types at a Glance

| Feature | Dental PPO (Most Common) | Dental HMO (Budget Option) | Indemnity (Most Flexible) |

|---|---|---|---|

| Average Monthly Premium | Medium ($30-$60) | Low ($10-$25) | High ($50-$80+) |

| Provider Choice | In-network or Out-of-network | In-network only | Any dentist |

| Deductible | Yes ($50-$100) | Usually None | Yes (Variable) |

| Annual Maximum | Yes ($1,000 – $2,000) | No Maximum | Yes (Variable) |

| Best For… | Balancing cost and choice | Saving on monthly bills | Keeping your current dentist |

The Price is Right (For You): Factors That Influence Your Cost

Why does your neighbor pay $30 a month for their plan while you’re quoted $55? The dental insurance average cost is just a starting point. Several personalized factors will determine your final premium.

-

Geographic Location: The cost of dental care varies wildly by region. A routine cleaning in Manhattan is simply more expensive than one in rural Kansas. Insurance companies adjust their premiums based on the cost of living and the average fees charged by dentists in your specific zip code.

-

The Generosity of the Plan: Not all PPOs are created equal. A plan with a low deductible ($50), a high annual maximum ($2,500), and orthodontic coverage for adults will have a much higher monthly premium than a basic plan with a $100 deductible and a $1,000 max.

-

Your Age: Age can be a factor, especially for children. Plans covering kids often include orthodontic benefits (braces), which increases the cost. For seniors, some plans are specifically designed to cover dentures and implants, which also affects pricing.

-

Waiting Periods: Some plans have waiting periods (e.g., you must wait 6 months for basic care and 12 months for major care). Plans with no waiting periods or very short ones are more desirable and, therefore, typically come with a higher monthly premium.

Cost vs. Value: Is Dental Insurance Worth It?

This is the million-dollar question. When you look at the math, you might think, “I pay $480 a year in premiums, and I only get two cleanings worth $300. Where’s the value?” That’s a valid point, but insurance is designed for the unexpected.

Here’s a simple way to look at the value:

Scenario A: The “Perfect Teeth” Year

-

Costs: You pay $50/month premium = $600/year.

-

Benefits Used: 2 cleanings + 1 set of x-rays = $350 value.

-

Outcome: You “lost” $250 on paper. However, you paid for peace of mind and preventative care that stopped small issues from becoming big, expensive ones. You also have coverage in case of an accident.

Scenario B: The “Unexpected Cavity” Year

-

Costs: You pay $600 in premiums.

-

Benefits Used: 2 cleanings ($300) + 2 fillings ($400 after insurance pays 80%) = $700 value.

-

Outcome: You “gained” $100 in value. The insurance helped you manage an unexpected cost.

Scenario C: The “Major Work” Year

-

Costs: You pay $600 in premiums.

-

Benefits Used: 2 cleanings ($300) + 1 crown ($600 after insurance pays 50%) = $900 value. (Plus, your insurance paid another $600 directly to the dentist).

-

Outcome: You received $1,500 worth of care for your $600 premium and $600 in copays. This is where insurance truly proves its worth.

The Bottom Line: If you only ever need preventative care, insurance might seem like a break-even or slight-loss proposition. But if you need a single filling, you’ve likely already recouped the cost of your premiums for the year. It’s a safety net against the high cost of unexpected dental problems.

Shopping Smart: How to Find the Best Plan for Your Budget

Ready to start looking? Here is a practical, step-by-step guide to finding a plan that fits your financial situation and dental needs.

-

Check Your Employer First: If you have a job, open enrollment is your golden ticket. Employer-sponsored plans are almost always the most affordable option because your company subsidizes the cost.

-

Assess Your Dental Health: Be honest with yourself. Do you have healthy teeth and just need maintenance? Look for a low-premium PPO with good preventative coverage. Do you have a history of cavities or need a crown soon? You’ll need a plan with a higher annual maximum and strong major care coverage, even if the premium is a bit higher.

-

Use Online Marketplaces: If you’re self-employed or your job doesn’t offer insurance, use reputable online comparison tools. The official health insurance marketplace for your state (from the Affordable Care Act) is one place to look, as dental coverage is often offered alongside medical plans. You can also use private brokers.

-

Read the Fine Print (The Summary of Benefits): Before you click “buy,” get the “Summary of Benefits and Coverage.” Don’t just look at the premium. Verify:

-

The deductible amount.

-

The annual maximum.

-

The coinsurance for basic and major care.

-

Any waiting periods for specific procedures.

-

Whether your current dentist is in the network.

-

Additional Paths to Affordable Dental Care

Maybe traditional insurance isn’t the right fit for you right now. Perhaps you’re between jobs, retired early, or simply find that the premiums don’t align with your needs. There are other legitimate ways to make dental care affordable.

-

Discount Dental Plans: These are not insurance. You pay a low annual membership fee (often under $150) and get access to a network of dentists who have agreed to provide services at a discounted rate (usually 10-60% off). You pay the dentist directly at the time of service. This can be a great option if you don’t have major dental issues and just want to save on routine and basic care.

-

Dental Schools: If you live near a university with a dental school, this can be a fantastic resource. Supervised dental students provide high-quality care at a fraction of the cost. The appointments take longer, but the savings can be substantial, especially for major work.

-

Government Programs: Medicare generally does not cover routine dental care, but Medicaid offers dental benefits for eligible low-income individuals and families. These benefits vary significantly by state, so check your state’s Medicaid website for details.

-

In-House Membership Plans: Many dental offices are now offering their own “membership” or “loyalty” plans. For a flat annual fee (e.g., $300), you get two cleanings, x-rays, and a discount on any other procedures performed at that office. It’s a simple, direct relationship between you and your dentist.

Conclusion

Understanding the dental insurance average cost is the first step toward taking control of your oral health without breaking the bank. While the average monthly premium for an individual usually falls between $20 and $60, the true cost of a plan is a combination of the premium, deductible, coinsurance, and annual maximum.

The best plan for you is the one that balances these factors against your personal dental history and financial comfort zone. Whether you opt for a flexible PPO, a budget-friendly HMO, or even a discount plan, the goal is the same: to make regular, preventative care affordable and to protect yourself from the high, unexpected costs of major dental work.

Remember, a healthy smile is an investment in your overall well-being. By doing your homework and asking the right questions, you can find a plan that keeps both your teeth and your finances in great shape.

Frequently Asked Questions (FAQ)

1. What is the average cost of dental insurance per month?

For an individual, you can typically expect to pay between $20 and $60 per month. Family plans range from $50 to $150 per month. The final cost depends on the type of plan (PPO, HMO) and the level of coverage.

2. Is dental insurance worth it if I have healthy teeth?

Yes, for most people it is. The premium you pay usually covers two preventative cleanings and exams per year, which can cost as much as the premium itself. More importantly, it acts as a safety net. If you were to crack a tooth or develop a cavity, your insurance would cover a large portion of that unexpected expense.

3. What is a “100-80-50” dental plan?

This is shorthand for a common coinsurance structure. It means the plan covers 100% of preventative care (like cleanings), 80% of basic care (like fillings), and 50% of major care (like crowns), after you have met your annual deductible.

4. What does “annual maximum” mean?

The annual maximum is the total dollar amount your insurance company will pay for your dental care in one year. For most plans, this is between $1,000 and $2,000. You are responsible for all costs after this limit is reached until the plan year resets.

5. Can I get dental insurance with no waiting period?

Yes, some plans offer no waiting periods for basic and even major care, but these plans typically have higher monthly premiums. It’s a trade-off between paying more now to have immediate coverage.

6. Does dental insurance cover braces?

Orthodontic coverage for braces is often an optional add-on or a feature of more comprehensive (and expensive) plans. If you need braces for a child or yourself, you must specifically look for a plan that includes orthodontic benefits, as it is not standard in most basic plans.

Additional Resource

For the most up-to-date and personalized information on health and dental coverage options in your state, a great place to start is the official government website:

Healthcare.gov: Dental Coverage in the Marketplace

(Please note: This is a general resource for U.S. readers. If you are in another country, please refer to your local health authority.)