There are few things more unsettling for a homeowner than the sound of a leak in the middle of a rainstorm—or the sight of a fallen branch protruding from your shingles. When disaster strikes, your mind immediately goes to two places: “How much will this cost to fix?” and “Will my insurance cover it?”

This is where the confusion begins. You call a contractor, and they give you a number. You call your insurance company, and they send an adjuster who gives you a different number. Suddenly, you are trapped in the middle of a financial tug-of-war, unsure of who is right and who is trying to take advantage of you.

Understanding the difference between a roof repair cost (what a contractor charges to do the physical work) and an insurance estimate (what the insurance company calculates the repair should cost) is the only way to navigate this process without losing your mind—or your money.

This guide will walk you through every nuance of these two numbers, explaining why they differ, how to handle the gap, and how to ensure your roof gets fixed properly without unnecessary financial strain.

Part 1: The Basics of Roofing Economics

Before we dive into the nitty-gritty of supplements and depreciation, we need to understand the fundamental business models of the two parties involved.

What is a “Roof Repair Cost”?

When a roofer gives you an estimate, they are not just selling you shingles. They are selling you a comprehensive service package that includes:

-

Materials: The physical products (shingles, underlayment, flashing, nails).

-

Labor: The wages for the crew. Roofing is dangerous, skilled labor.

-

Overhead: The cost of running a business—insurance (liability and worker’s comp), trucks, fuel, dumpster fees, marketing, and office staff.

-

Profit Margin: The money the business needs to make to stay afloat and handle future warranty claims.

A contractor’s price is based on the real world. It costs what it costs to get a crew to your house, safely remove the old roof, and install a new one that won’t leak.

What is an “Insurance Estimate”?

An insurance estimate is generated by a claims adjuster (either employed by the insurance company or an independent adjuster hired by them). They use specialized software—most commonly Xactimate or Symbility.

These programs are essentially complex pricing databases. They assign a specific price to every single task involved in a roofing job, from tearing off old shingles to disposing of debris and installing new drip edge. The prices are generally based on regional averages.

The goal of the initial insurance estimate is to provide a “reasonable” cost to repair or replace the roof based on industry standards. However, it is crucial to understand that this is an opening offer, not necessarily the final payment.

Part 2: The Anatomy of a Discrepancy

So, why are these two numbers often different? If everyone is using the same software, shouldn’t they match? Not exactly. Here is why the gap exists.

The “Retail vs. Insurance” Pricing Model

This is the most common reason for a mismatch.

-

Contractor Pricing: Retail. If you called a roofer and said, “I want a new roof, no insurance involved,” they would give you a retail price. This price accounts for the fact that the job might be small, might be complicated, and needs to cover their overhead for the month.

-

Insurance Pricing: Wholesale/Replacement Cost. Insurance pricing is often based on replacement cost value (RCV) minus depreciation. The software prices are usually fair market rates, but they don’t always account for the “hassle factor” of a small repair or the premium prices charged by the only available contractor in a post-storm area.

Line Item Discrepancies

The difference is rarely a single big number; it is usually a collection of small disagreements. Common points of contention include:

-

Underlayment: Did the adjuster price standard felt paper, but your local code requires synthetic underlayment?

-

Flashing: Did the adjuster account for replacing all the step flashing around the chimney, or only what is visible?

-

Decking: Does the estimate account for the possibility of rotten plywood underneath? (Insurance usually covers this, but they wait until it’s discovered).

-

Code Upgrades: If your roof needs to be brought up to current building codes (like ice and water shield in valleys), insurance may or may not cover the full cost, depending on your policy.

The “Supplement” Explanation

When a contractor says they are going to “fight the insurance company,” what they really mean is they are going to file a supplement. A supplement is essentially a change order to the insurance claim. The contractor sends their detailed bid to the insurance adjuster, pointing out the missing items, incorrect measurements, or necessary code upgrades. If the adjuster agrees, they issue a second check.

Part 3: Comparative Analysis: Repair vs. Estimate

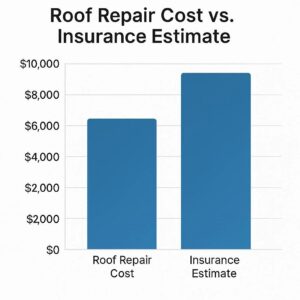

To visualize this battle of numbers, let’s look at a hypothetical scenario. Imagine a medium-sized roof (30 squares) that has suffered moderate wind and hail damage.

Hypothetical Breakdown of Costs

| Line Item | Initial Insurance Estimate (Adjuster) | Contractor’s Repair Bid (Retail) | Explanation of Difference |

|---|---|---|---|

| Tear-off (Labor) | $1,800 | $2,200 | Contractor uses a premium crew; adjuster uses average rates. |

| Shingles (Materials) | $5,000 | $5,300 | Contractor may use a specific brand with higher margins. |

| Underlayment | $400 (Standard Felt) | $800 (Synthetic) | Local code requires synthetic; adjuster priced basic felt. |

| Flashing | $300 | $700 | Adjuster missed replacing the chimney step flashing. |

| Dumpster / Disposal | $400 | $600 | Rising fuel and dump fees not yet reflected in software. |

| Drip Edge | $0 | $450 | Adjuster said it was fine; code requires replacement on re-roof. |

| Sales Tax | $0 | $400 | Adjuster forgot to calculate tax; contractor must pay it. |

| Overhead & Profit (O&P) | $0 | $1,500 | Only included if a “General Contractor” is needed per policy. |

| Total | $7,900 | $11,950 | Discrepancy of $4,050 |

Reading the Table

As you can see, the insurance adjuster wasn’t necessarily “lowballing” the homeowner. They were pricing based on a standard, by-the-book estimate. The contractor, however, priced the job based on what they knew it would actually take to get the roof permitted, passed inspection, and warrantied. The gap of $4,050 is what the contractor must recover through the supplement process.

Part 4: Navigating the Claims Process

So, you have two numbers. What do you do now? The process is a dance, and you need to lead.

Step 1: Do Not Sign an AOB (Assignment of Benefits) Immediately

In the first 24 hours after a storm, you may have a contractor knock on your door asking you to sign an Assignment of Benefits (AOB). This legally allows them to speak to your insurance company on your behalf and often allows them to collect the check directly.

Warning: Be very careful with this. While some reputable contractors use AOBs for convenience, others use them to inflate prices and sue your insurance company, which can eventually raise your rates. Get multiple opinions first.

Step 2: Hire a Reputable Local Contractor Before You Cash the Check

Many homeowners make the mistake of cashing the insurance check and then trying to find a contractor. Once that check is cashed, the insurance company considers the matter settled.

Instead, find your contractor first. Have them inspect the roof alongside you (or after the adjuster leaves). Ask them:

-

“Does the insurance estimate cover everything I need?”

-

“Are there any line items missing?”

-

“Will you handle the supplement process for me?”

Important Note: Most reputable roofing companies have dedicated “claims specialists” who handle supplements for free. They want to get paid, so it is in their interest to help you maximize your claim.

Step 3: Understanding the Two-Check System (Mortgage Companies)

If your roof is damaged, your insurance claim check is often made out to both YOU AND YOUR MORTGAGE LENDER. This is because the lender has a financial interest in the property.

-

First Check (ACV): This is the Actual Cash Value check. It is the replacement cost minus depreciation. This check is usually smaller. You can cash this one to start the work.

-

Second Check (RCV): This is the recoverable depreciation. You only get this money AFTER the work is completed and the insurance company receives a “Certificate of Completion” or final invoice from the contractor proving the roof is done.

The Flow of Money

| Phase | Who Gets Paid | Amount | Condition |

|---|---|---|---|

| Initial Claim | Homeowner & Lender | Actual Cash Value (ACV) | Roof is damaged. Claim approved. |

| Contractor Hired | Contractor (via homeowner) | ACV Check (plus any deductible) | Contract signed; materials ordered. |

| Work Completed | Contractor (final payment) | Recoverable Depreciation | Insurance inspects finished work; releases second check to homeowner/lender. |

| End Result | Contractor is paid in full | Replacement Cost Value (RCV) | Homeowner’s roof is fixed; policy continues. |

Part 5: Hidden Variables That Affect the Bottom Line

Beyond the basic numbers, several factors can influence the final cost vs. the estimate.

1. The Age of Your Roof

If your roof is older than 20 years, many insurance companies will only pay for the Actual Cash Value (ACV), not the full replacement cost. If your roof is old and damaged, you might get a check for very little, leaving you to pay the majority of the cost yourself.

2. Demand Surge

After a major hurricane or hailstorm, the cost of labor and materials in a specific region can spike. This is called “Demand Surge.” Insurance companies are usually aware of this and have mechanisms to adjust their estimates, but it often takes a contractor’s higher bid to trigger the recognition of the surge.

3. Material Availability

Supply chain issues can mean you cannot get the specific shingle color the adjuster priced. If you have to buy a premium “architectural” shingle because the standard one is backordered for six months, the price difference needs to be supplemented.

4. The Deductible

Your deductible is the amount you are responsible for paying out of pocket.

-

If repair cost is $10,000 and deductible is $1,000: The insurance pays $9,000, you pay $1,000.

-

If the estimate is $8,000 but the contractor charges $10,000: You must bridge the $2,000 gap, or the contractor must get the insurance to supplement the missing $1,000 (on top of your deductible).

Warning on Deductibles: Be wary of contractors who offer to “waive” your deductible. This is insurance fraud in most states. It artificially inflates the cost of the claim and is illegal. If a contractor offers this, run the other way.

Part 6: When the Numbers Don’t Match (And How to Fix It)

You have the insurance check. The contractor’s price is higher. Here is your path forward.

The Contractor’s Role: The Supplement

As mentioned, the contractor should submit a supplement. They will provide:

-

Photos: Showing missing flashing, rotten decking, or complex roof angles the adjuster missed.

-

Invoices: Proving the cost of materials has gone up.

-

Code Enforcement: A letter from the local building department stating what is required by law.

The insurance adjuster reviews this. If approved, they issue a supplemental payment.

The Homeowner’s Role: Public Adjusters

If the contractor and the insurance company cannot agree, you might need to bring in a Public Adjuster.

-

What they do: A public adjuster works for you, not the insurance company. They re-inspect the roof, re-write the estimate, and negotiate with the insurance company on your behalf.

-

The Cost: They typically charge a percentage of the final claim payout (usually 10-20%).

-

When to use them: If the claim is large, complex, or if the insurance company is being unreasonable. For a simple repair, a good contractor should handle it.

Part 7: FAQ: Roof Repair Cost vs Insurance Estimate

Q1: My insurance adjuster gave me an estimate, but my roofer says it’s too low. Is the roofer just trying to rip me off?

Not necessarily. The roofer is looking at physical conditions the adjuster may have missed from the ground or from a quick walk. Ask the roofer to point out specifically what the adjuster missed. If they can show you missing items (like damaged flashing or the need for ice and water shield), they are likely being honest.

Q2: Can I keep the money if I don’t fix the roof?

If you have a mortgage, the check is likely made out to you and the lender, so you cannot cash it without the lender’s endorsement. They will require proof the work is done. If you own the home outright, technically, the money is yours, but not fixing a known damage claim can lead to your insurance policy being canceled or non-renewed at the next renewal.

Q3: What is “Recoverable Depreciation”?

It is the amount of money the insurance company holds back until the work is done. For example, if your roof is valued at $10,000 but is 5 years old, they might depreciate it 10%, sending you an ACV check for $9,000. The $1,000 they hold is the “recoverable depreciation.” You get it when the roof is finished.

Q4: Do I have to use a contractor approved by my insurance company?

No. You have the right to choose your own contractor. The insurance company cannot force you to use their preferred vendor. However, using a reputable contractor often makes the supplement process smoother.

Q5: My roof is leaking, but insurance only covers “sudden and accidental” damage. Will they pay for age-related leaks?

Generally, no. Insurance covers perils like wind, hail, and fire. If your roof is leaking because it is 25 years old and simply worn out, that is considered “wear and tear” or “maintenance,” which is not covered. You would be responsible for the full repair cost.

Conclusion

Navigating the difference between a roof repair cost and an insurance estimate doesn’t have to be a battle. The key takeaway is that the insurance estimate is a starting point, not the final word. Contractors look at the physical reality of your roof, while adjusters look at a software screen.

By understanding the roles of depreciation, code upgrades, and the supplement process, you empower yourself to advocate for a fair settlement. Always hire a reputable local contractor before you settle with the insurance company, and never be afraid to ask questions. A successful claim is one where the roof is fixed properly, the contractor is paid fairly, and the homeowner is left with a dry house and peace of mind.

Additional Resource

For further reading on consumer rights and navigating the insurance claims process, visit the National Association of Insurance Commissioners (NAIC) website. They provide state-specific guides and resources to help you understand your policy and file complaints if necessary.

[Link to NAIC Consumer Resources] (https://content.naic.org/consumer.htm)