Let’s be real for a second: car insurance can feel like a giant mystery. You pay your premium every month, hoping you never have to use it, but you’re never quite sure if you’re paying the right price. If you’ve ever chatted with friends about your rates, you’ve probably noticed something strange. Your friend who lives just twenty miles away might be paying hundreds of dollars less than you for the exact same coverage. Why? More often than not, the answer comes down to a few simple digits: your zip code.

In the United States, where you park your car at night is one of the most powerful factors influencing your insurance premium. It doesn’t matter if you have a perfect driving record; if you live in a postal code with high levels of traffic, crime, or costly repairs, you will pay more.

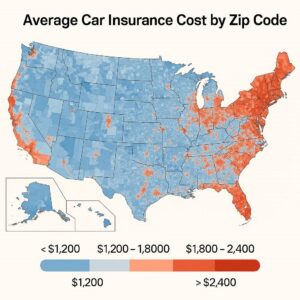

In this guide, we are going to peel back the curtain on the Average Car Insurance Cost by Zip Code Across the United States. We’ll explore why location matters so much, look at the national trends, and give you the tools you need to navigate the market and find the best coverage for your address.

Average Car Insurance Cost by Zip Code Across the United States

Why Your Zip Code Matters More Than You Think

Before we dive into the specific numbers, it’s important to understand the “why.” Insurance is a business of risk. When an insurance company decides how much to charge you, they are essentially calculating the likelihood that they will have to pay out money on your behalf. Your zip code acts as a shortcut for them to understand the environment your car lives in 24/7.

Think of it this way: you aren’t just insuring yourself; you are buying into a risk pool of everyone in your general area. If that pool is expensive to insure, your rates go up.

The Main Factors Tied to Your Location

Insurance companies look at a massive amount of data tied to specific geographic areas. Here are the primary reasons your address dictates your rate:

-

Traffic Density and Congestion: This is a big one. The more cars on the road, the higher the chance of an accident. If you live in a densely populated urban core like Los Angeles, Chicago, or New York City, you are statistically more likely to be involved in a fender bender than someone living in a rural town in Montana. More accidents mean more claims, and those costs are distributed among the drivers in that area.

-

Crime Rates: Insurers closely monitor local crime statistics. Areas with higher rates of vehicle theft, vandalism, and break-ins are significantly more expensive to insure. If your car is more likely to be stolen or broken into, the insurer needs to charge a premium to cover that potential loss.

-

Cost of Repairs and Medical Care: Where you live affects how much it costs to fix a car or treat an injury. In wealthy suburbs or major cities, labor rates at auto body shops and medical facilities are often higher. If an accident happens in an area with high labor rates, the insurance company’s bill will be higher, and they adjust premiums accordingly.

-

Weather Patterns: Are you in Tornado Alley? Do you live on the hurricane-prone Gulf Coast? Or perhaps an area known for massive hailstorms? Your zip code dictates the likelihood of your car being damaged by a natural disaster. Insurers factor in these catastrophic risks, which is why rates in Florida and parts of Texas can be so volatile.

-

Uninsured Motorist Statistics: Sadly, not everyone on the road has insurance. Insurers track the rate of uninsured drivers by region. If you live in an area with a high percentage of uninsured motorists, your premium will likely go up. This is because if an uninsured driver hits you, your own insurance company has to cover the damages under your uninsured motorist coverage.

Important Note: While your zip code is a major factor, it works in tandem with your personal details—your age, driving history, credit score (in most states), and the type of car you drive—to create your final rate.

National Overview: A Tale of Three Digts

It’s impossible to list every single zip code in the United States—there are over 40,000 of them! However, we can look at general trends to understand the landscape. The difference in cost between the cheapest and most expensive areas can be shocking, often varying by thousands of dollars per year.

Generally speaking, insurance rates form a kind of geographic hierarchy:

-

Urban Cores (Highest Cost): Dense city centers almost always command the highest premiums due to congestion, theft, and vandalism.

-

Suburban Rings (Moderate Cost): As you move away from the city center, rates tend to drop. There’s less traffic and often lower crime, offering a nice balance.

-

Rural Areas (Lowest Cost): Wide-open spaces with minimal traffic and low crime rates typically enjoy the lowest insurance costs in the country.

Let’s look at a comparative snapshot to illustrate these differences.

Comparative Table: Estimated Monthly Premiums by Location Type

*The following figures are estimates for a standard policy with full coverage for a 35-year-old driver with a good driving record. Actual rates will vary.*

| Location Type | Example Area | Estimated Monthly Premium (Full Coverage) | Primary Risk Factors |

|---|---|---|---|

| Major Urban Core | Downtown Detroit, MI | $300 – $450+ | Very high theft rates, high uninsured motorist population, urban congestion. |

| Dense Metropolis | Brooklyn, NY | $250 – $400 | Extreme traffic density, high cost of repairs, high risk of vandalism/parking damage. |

| Large City | Downtown Houston, TX | $200 – $300 | Heavy traffic, severe weather (hurricanes, hail), high litigation rates. |

| First-Ring Suburb | Cook County, IL (outside Chicago) | $150 – $220 | Moderate congestion, proximity to city risks, moderate theft. |

| Mid-Sized City | Oklahoma City, OK | $130 – $180 | Susceptibility to hailstorms, moderate traffic, average crime. |

| Small Town | Bend, OR | $110 – $150 | Lower traffic density, lower crime, lower cost of living. |

| Rural Community | Rural Vermont | $80 – $120 | Very low traffic, low crime, minimal congestion. |

As you can see, the simple act of moving from a rural area to a downtown core can more than triple your insurance bill.

Deep Dive: Regional Hotspots and Surprising Trends

Let’s take a closer look at specific regions and states where zip code plays a particularly dramatic role.

The High-Stakes Game of Urban Living: Detroit and NYC

When discussing the Average Car Insurance Cost by Zip Code Across the United States, two cities inevitably dominate the conversation: Detroit, Michigan, and New York, New York.

Detroit, Michigan: For years, Detroit has held the unenviable title of the most expensive place in the U.S. to insure a car. Why? It’s a perfect storm of negative factors.

-

High Theft: The city has historically struggled with high vehicle theft rates.

-

High Uninsured Rate: A significant portion of drivers are uninsured, shifting costs onto those who are insured.

-

No-Fault Laws: Michigan had, until recently, the most generous (and expensive) unlimited lifetime medical benefits under its no-fault insurance system. While reforms have helped lower rates slightly, they remain astronomically high compared to the rest of the nation. A driver in a good zip code in the suburbs of Detroit pays far less than a driver in the city center, but both pay more than similar drivers in other states.

New York, New York: Living in the five boroughs is a financial commitment in every way, and insurance is no exception. A zip code in Manhattan or Brooklyn will carry a hefty premium. The primary culprit here isn’t necessarily high-speed collisions, but the sheer volume of vehicles. The constant stop-and-go traffic leads to a high frequency of minor accidents. Furthermore, parking is a nightmare; the risk of your car being hit while parked, vandalized, or stolen is simply much higher in such a dense environment.

The Sunshine State Struggle: Florida

Florida presents a unique case study. You might think that wide, sunny roads would lead to cheap insurance, but the opposite is true. Florida is one of the most expensive states in the nation, and it’s all down to a different set of factors.

-

Weather: The state is ground zero for hurricanes and tropical storms. Every year, thousands of vehicles are flooded or damaged by wind and debris.

-

Fraud and Litigation: For a long time, Florida was notorious for a specific type of fraud: staged accidents and questionable medical claims leading to lawsuits. This created a litigation-heavy environment where insurance companies spent as much on legal fees as they did on claims. While recent legal reforms aim to curb this, the impact is still baked into current rates.

-

High Concentration of Drivers: With a massive population of both permanent residents and seasonal “snowbirds,” the roads are perpetually busy, especially during winter months.

If you look at a map of Florida insurance rates, you’ll see a clear gradient. Zip codes right along the coast, especially in South Florida (Miami-Fort Lauderdale), are the most expensive, while those further inland in North Florida are comparatively cheaper.

The Affordable Havens: Rural Heartland and Mountain States

On the flip side, the most affordable zip codes in the country are generally found in rural areas with low population density and minimal severe weather.

-

Idaho and Iowa: These states consistently rank among the cheapest for car insurance. They offer a combination of low crime rates, sparse traffic, and less exposure to catastrophic weather events like hurricanes or earthquakes.

-

Rural Maine, Vermont, and New Hampshire: Northern New England offers some of the most affordable rates east of the Mississippi. The quiet, rural nature of these states means fewer claims, which translates directly to lower premiums for drivers.

-

The Rural Midwest: Vast stretches of Kansas, Nebraska, and the Dakotas offer very low rates. While they do face risks like blizzards and the occasional tornado, the wide-open spaces and low population density keep accident rates down.

How to Navigate Rates in Your Specific Zip Code

Okay, so you can’t just pack up and move to rural Idaho to save a few hundred bucks on car insurance. You’re stuck with your zip code, for now. So, what can you do to make sure you’re getting the best possible rate within your specific area? Plenty.

Don’t Just Accept the First Quote

Loyalty doesn’t pay in the insurance world. Insurance companies use proprietary algorithms to assess risk. One company might weigh credit scores heavily, while another might be more forgiving of a slightly older driving infraction. Because of these different “appetites” for risk, rates for the exact same driver and the exact same zip code can vary wildly from one company to the next.

Actionable Tip: You should shop around for car insurance at least once a year, or whenever your policy is up for renewal. Get quotes from at least three different providers. Use independent agents who can quote you from multiple companies at once.

Leverage Usage-Based Insurance

One of the most effective ways to fight back against a “bad” zip code is to prove that you, personally, are a safe driver. Many major insurers now offer usage-based insurance (UBI) programs. These involve a mobile app or a small device plugged into your car that monitors your driving habits.

-

How it helps: The insurer tracks things like hard braking, rapid acceleration, time of day you drive, and miles driven. If you live in a high-risk city but drive conservatively and only on weekends, a UBI program can prove you are not the “average” risk for your zip code.

-

The Trade-off: It requires you to share your driving data, which some people are uncomfortable with. Also, very poor driving habits could theoretically raise your rate.

Maximize Every Discount Available

Insurance companies have a long list of discounts, and you need to make sure you are getting every single one you qualify for. This is a simple way to chip away at that zip-code-driven premium.

Helpful List: Common Discounts to Ask About

-

Bundling: Do you have your home or renters insurance with the same company? If not, combine them. This is often the single biggest discount available.

-

Good Driver: A clean driving record for 3-5 years should qualify you for a significant discount.

-

Low Mileage: If you work from home or live close to work, you might qualify for a low-mileage discount. Fewer miles on the road equals less risk.

-

Vehicle Safety Features: Cars with anti-lock brakes, anti-theft devices, and advanced driver-assistance systems (like lane-keep assist) often qualify for discounts.

-

Defensive Driving Course: Some insurers offer a discount for completing an approved defensive driving or mature driver improvement course.

-

Paid-in-Full: If you can afford to pay your six-month or annual premium upfront, you can often save on installment fees.

Reassess Your Coverage Needs

This is a big one. If you are driving an older car that is paid off, you might not need “full coverage” (which typically means comprehensive and collision). Take a hard look at your car’s actual cash value. If your car is only worth $3,000, and your deductible is $1,000, is it worth paying hundreds of dollars a year for collision coverage? If you got into an at-fault accident, the insurance company would likely just total the car and give you a check for its value minus your deductible. You might be better off dropping that coverage and banking the savings to put toward your next car.

Crucial Advice: Before dropping collision or comprehensive coverage, make sure you have the financial means to replace your car if it is totaled in an accident you cause. This is a risk vs. reward calculation you have to make for yourself.

The Future of Zip Code Rating

The system isn’t static. The way insurers use location is evolving. With the rise of electric vehicles (EVs) and advanced driver-assistance systems (ADAS), the cost to repair cars is skyrocketing. A simple fender bender in a new car loaded with sensors can cost tens of thousands of dollars to fix. This means that zip codes with a high concentration of new, expensive cars might see their rates increase even faster than others, as the “average cost of repair” for that area climbs.

Furthermore, climate change is forcing insurers to constantly update their risk models. Zip codes that were once considered safe from wildfires or flooding are now being re-evaluated. We may see a future where “climate risk” becomes an even more dominant factor in determining your premium than traffic density.

Conclusion

Understanding the Average Car Insurance Cost by Zip Code Across the United States reveals just how personalized this expense truly is. While you cannot change your zip code to instantly lower your bill, you can change how you approach the market. Your location sets the stage, but your choices—from the coverage you select to the company you shop with—determine the final price you pay. By staying informed, shopping around, and taking advantage of the tools and discounts available, you can ensure that no matter where you live, you are getting the best possible value for your hard-earned money.

Frequently Asked Questions (FAQ)

1. Why do insurance companies use zip codes? Isn’t that unfair?

Insurance companies use zip codes because statistical data shows a strong correlation between location and risk. It’s not about judging individuals, but about predicting the likelihood of claims in a specific geographic area. It allows them to accurately price policies based on the very real risks associated with where a car is parked and driven most often.

2. If I move to a new zip code, when will my rate change?

You should inform your insurance company immediately when you move. Your rate will typically be recalculated based on your new zip code starting on the effective date of your move. You might receive a refund or owe additional money depending on whether your new location is cheaper or more expensive.

3. Is it legal for insurance companies to use zip codes?

Yes, it is legal in all 50 states. However, some states have regulations that limit how much weight insurers can put on certain geographic factors or require them to justify significant rate differences between neighboring zip codes.

4. Can my credit score affect my rate more than my zip code?

In most states (excluding California, Hawaii, Massachusetts, and Michigan), yes, your credit-based insurance score can be a very powerful factor. Insurers have found a strong correlation between credit history and the likelihood of filing a claim. For many people, improving their credit score can lead to significant savings, sometimes even offsetting the impact of a high-risk zip code.

5. I live in an expensive city. Should I just get the state minimum coverage to save money?

This is generally a bad idea. If you are in an at-fault accident, state minimum limits are often far too low to cover the damages, especially for medical bills. You could be sued personally for the difference, putting your wages and assets at risk. It’s usually wiser to carry higher liability limits, even if it means paying a bit more now, to protect yourself from financial disaster later.