There are few milestones in a teenager’s life as significant as getting a driver’s license. It represents freedom, independence, and a step toward adulthood. However, for parents, this milestone is often accompanied by a moment of sticker shock when they contact their insurance provider. Adding a 16-year-old to a car insurance policy is notoriously expensive, and understanding why—and how much it will actually cost—is the first step in managing your family’s budget.

The simple truth is that car insurance premiums are based on risk, and statistically, 16-year-olds are the highest-risk demographic on the road. Their lack of experience, combined with statistics showing higher accident rates, forces insurance companies to adjust premiums accordingly.

But what does that look like in real numbers? You are not just looking for a vague estimate; you need a concrete figure to budget for. In this comprehensive guide, we will break down the average cost to add a 16-year-old to car insurance, explore the variables that influence that price, and provide actionable strategies to lower your bill without sacrificing coverage.

Average Cost to Add a 16-Year-Old to Car Insurance

Quick Overview: The National Average

Before diving into the nuances, let’s look at the baseline. According to industry data and actuarial tables, adding a 16-year-old to a standard auto insurance policy causes premiums to increase significantly.

-

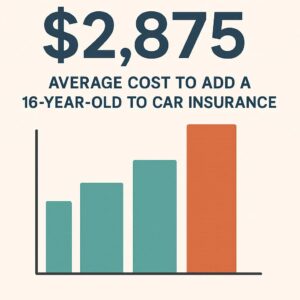

Average Annual Increase: Adding a teen driver typically raises a parent’s annual premium by $2,000 to $3,500.

-

Monthly Impact: This translates to roughly $170 to $300 extra per month.

To put this in perspective, you might currently pay $1,500 per year to insure two adult drivers. Adding a 16-year-old could triple that cost, bringing the total to $4,500 or more annually. While these numbers can be alarming, they are the reality of insuring a new driver.

Important Note: These are national averages. Your actual rate could be significantly higher or lower depending on where you live, the car your teen drives, and the insurance company you choose.

Why Is It So Expensive to Insure a 16-Year-Old?

To understand the cost, you have to understand the “why.” Insurance is a business of probability. Insurers pool risk among thousands of policyholders, and the premiums paid by the many cover the claims made by the few.

The Statistics Don’t Lie

The Centers for Disease Control and Prevention (CDC) provides sobering statistics that directly impact insurance premiums:

-

Teen drivers ages 16 to 19 are nearly three times more likely to be in a fatal crash than drivers aged 20 and older.

-

The risk of motor vehicle crashes is higher among 16-17-year-olds than among 18-19-year-olds.

-

Per mile driven, teen drivers are involved in significantly more accidents than adults.

Because the likelihood of a claim is statistically much higher, the cost to provide coverage must also be higher. When you add a teen, you are essentially asking the insurance company to take on a much larger financial risk.

The “New Driver” Factor

A 16-year-old has just begun to understand the dynamics of driving. They are learning to judge distances, react to hazards, and manage distractions. This lack of experience is the single biggest factor in the premium increase. Even the most responsible and mature 16-year-old is still statistically grouped with every other driver in their age bracket.

Average Cost Breakdown: By the Numbers

While the national average gives you a starting point, it is more helpful to see how these costs break down in different scenarios. Let’s look at a hypothetical but realistic example.

Scenario: A married couple in their 40s, both with clean driving records, living in a suburban area of Ohio. They currently drive a 2020 Honda Accord and a 2018 Toyota RAV4. Their current annual premium is $1,800.

Here is how adding their 16-year-old son or daughter changes the bill.

| Scenario | Annual Premium | Increase Over Base | Reasoning |

|---|---|---|---|

| Parents Only (Current) | $1,800 | N/A | Base rate with multi-car and safe driver discounts. |

| Add 16-Year-Old to Parents’ Policy | $4,500 | +$2,700 | Teen is rated as an occasional driver on the existing vehicles. |

| Add 16-Year-Old as Primary Driver of a 2023 Sports Coupe | $7,200 | +$5,400 | Teen is the primary driver of a high-performance, expensive-to-repair vehicle. |

| Add 16-Year-Old to Parents’ Policy (with Good Student Discount) | $3,960 | +$2,160 | A 20% good student discount is applied to the teen’s portion of the premium. |

As you can see, the variables can swing the final cost by thousands of dollars. The key takeaway here is that you have a significant amount of control over the final price.

Key Factors That Influence the Cost

Insurance companies use a complex algorithm to determine your premium. When adding a 16-year-old, several specific variables carry extra weight.

1. The Car They Drive

This is perhaps the biggest lever you can pull.

-

Safe and Sensible Vehicles: Putting your teen on an older, safe, but low-power vehicle like a Honda CR-V, Subaru Outback, or Toyota Camry will keep costs lower. These cars are cheap to repair and not associated with risky driving behavior.

-

Vehicles to Avoid: Sports cars, high-performance muscle cars, and large, luxury SUVs will trigger massive premium hikes. Insurers look at the vehicle’s horsepower, repair costs, and theft rate. A Ford Mustang or a brand-new BMW will cost a fortune to insure for a 16-year-old.

2. Location, Location, Location

Where you park the car at night matters.

-

Urban vs. Rural: A family living in a densely populated city like Los Angeles or New York will pay significantly more than a family in a rural town in Iowa. Higher traffic density leads to a higher probability of accidents.

-

State Regulations: Minimum coverage requirements vary by state. Some states also allow insurers to use credit scores as a factor in pricing, which can impact rates differently depending on your financial profile.

3. Gender of the Teen

Statistically, male drivers under the age of 20 are involved in more accidents and more severe accidents than their female counterparts.

-

Males: Typically see the highest rates. The increase for a 16-year-old male can be 10-15% higher than for a female of the same age.

-

Females: While still high, rates for female teens are generally slightly lower. This gap narrows as drivers get older and more experienced.

4. Coverage Levels and Deductibles

If you choose to add your teen and maintain high coverage limits with a low deductible ($250 or $500), your premium will be higher. While it is not wise to strip your coverage to dangerous lows just to afford adding a teen, you can adjust your deductibles to find a middle ground. Opting for a $1,000 deductible, for example, can lower the annual premium.

5. The Insurance Company Itself

Not all insurers treat teen drivers equally. Some companies are known for being more “parent-friendly” and offer competitive rates for families, while others penalize teen drivers more harshly. This is why shopping around is essential.

Comparing Coverage Options: To Add or Not to Add?

When your 16-year-old gets their license, you have a few distinct paths you can take regarding insurance. It is crucial to understand the implications of each.

Option A: Add Them to Your Existing Policy

This is the most common and usually the most cost-effective route.

-

Pros: You consolidate your business with one carrier, which often unlocks multi-car or multi-policy discounts. It simplifies billing and ensures your teen has adequate coverage.

-

Cons: Your premium will increase substantially. If your teen has an accident, it goes on your record and could affect your rates for years.

Option B: Get Them a Separate Policy

In theory, you could buy a completely separate policy for your teen.

-

Pros: It shields your driving record from theirs. If they have an accident, your personal rates might not be directly impacted upon renewal (though the company may still be aware).

-

Cons: It is almost always significantly more expensive. A young driver on their own policy does not benefit from the multi-policy discounts, homeowner bundling, or the “experienced operator” rating that comes with being on a parent’s policy. You could easily pay twice as much for a standalone policy.

Option C: Exclude Them from the Policy

Some insurers allow you to specifically exclude a licensed driver in the household.

-

Pros: Your premium does not increase.

-

Cons: If your 16-year-old drives any car—even in an emergency—and gets into an accident, the insurance company will deny the claim entirely. You would be personally responsible for all damages, injuries, and legal fees. This is financially catastrophic and is rarely a good idea.

Important Note: If a licensed 16-year-old lives in your house, most insurance companies require you to inform them. Trying to hide a teen driver to save money is considered fraud and can lead to a canceled policy or denied claims.

Proven Strategies to Lower Your Costs

Paying full price for teen insurance is not mandatory. Here are the most effective ways to reduce the financial burden.

1. Leverage Every Available Discount

Insurance companies offer a variety of discounts that specifically target young drivers. You must ask your agent about them.

-

Good Student Discount: This is the most common and valuable discount. If your teen maintains a B average or a GPA of 3.0 or higher, you can save up to 15-20% on the premium. Insurers view good students as more responsible.

-

Driver Training Discount: Completing an approved driver’s education course, beyond what is required for the license, can net a small discount.

-

Student Away at School: If your teen goes to college more than 100 miles away and does not take a car, you can often get a significant discount. Since they are not at home to drive the car, the risk is lower.

2. Choose the Right Vehicle (The “Beater” Car Debate)

There is a common myth that giving your teen a cheap, old “beater” car is the cheapest option for insurance. This is not always true.

-

Liability Only: If the car is worth less than $3,000-$4,000, you can drop the comprehensive and collision coverage. This drastically reduces your cost because you are only paying for liability.

-

Safety Matters: A slightly older car (5-8 years old) with modern safety features (side airbags, electronic stability control) but a low cash value is the sweet spot. It protects your child but won’t cost a fortune to insure.

3. Increase Your Liability Umbrella

While this sounds counterintuitive to lowering costs, consider this: if your teen is at fault in a serious accident, you could be sued for millions. Raising your liability limits to $500,000 or $1,000,000 is relatively inexpensive. Alternatively, purchasing a separate Umbrella Policy provides an extra layer of multi-million dollar protection for your family assets. This doesn’t lower your auto bill, but it protects your savings.

4. Utilize Telematics (Usage-Based Insurance)

Most major insurers now offer programs where you install a small device in the car or use a smartphone app to monitor driving habits (e.g., Progressive’s Snapshot, Allstate’s Drivewise, State Farm’s Drive Safe & Save).

-

How it helps: These programs track hard braking, speeding, fast cornering, and the time of day the car is driven.

-

The Incentive: If your teen drives safely, you can earn substantial discounts (often 10-30%). However, be aware that if the data shows risky driving, your rates could go up or the discount could be withheld. This is an excellent tool to encourage good habits.

5. Review Your Coverage Limits

When adding a teen, it is a good time to review your entire policy.

-

Drop Collision on Older Cars: As mentioned above, if the car’s value is low, paying for collision coverage might not make financial sense.

-

Bundle and Save: Ensure your auto insurance is bundled with your homeowners or renters insurance for the maximum multi-policy discount.

Real-World Scenarios: What Other Families Pay

To make this even more realistic, here are three distinct family profiles and what they might expect to pay.

Family A: The Suburban Planners

-

Location: Suburbs of Atlanta, GA.

-

Parents’ Cars: 2021 Honda Pilot, 2019 Mazda CX-5.

-

Teen: 16-year-old male.

-

Strategy: Added to parents’ policy, drives the Mazda CX-5 occasionally. Good student discount applied.

-

Estimated Annual Increase: $2,900

Family B: The Rural Dependables

-

Location: Rural Nebraska.

-

Parents’ Cars: 2015 Ford F-150, 2018 Chevrolet Equinox.

-

Teen: 16-year-old female.

-

Strategy: Added to parents’ policy. She is the primary driver of the Equinox. Completed a driver’s ed course.

-

Estimated Annual Increase: $1,900

Family C: The Urban High-Risk

-

Location: Downtown Chicago, IL.

-

Parents’ Cars: 2023 Tesla Model 3 (leased), 2022 BMW X5.

-

Teen: 16-year-old male.

-

Strategy: Added to parents’ policy. He will be an occasional driver of the BMW. No good student discount. High coverage limits required by the leases.

-

Estimated Annual Increase: $5,500+

These scenarios illustrate the massive range of possibilities. The family in rural Nebraska pays less because the risk environment is lower, while the urban family with luxury vehicles pays a premium for the high cost of repairs and the urban setting.

The Long-Term View: What Happens at 17, 18, and Beyond?

The good news is that this high cost is not permanent. Insurance premiums are heavily weighted by age. As your teen gains experience and moves through their teenage years, the price will gradually drop.

-

Age 17: A slight decrease. One year of accident-free driving helps, but they are still statistically high-risk.

-

Age 18: A more noticeable drop, especially if they are also a student away at college.

-

Age 19: Continued decrease.

-

Age 25: This is the magic number. At 25, drivers are no longer considered “young” and rates typically drop significantly, assuming a clean record.

The single best thing your teen can do to lower costs in the long run is to maintain a clean driving record. No tickets, no accidents. One at-fault accident can keep rates elevated for three to five years, negating the “aging out” process.

Conclusion

Adding a 16-year-old to your car insurance is a significant financial event, with the average cost ranging from $2,000 to $3,500 per year. While the price is driven by undeniable statistics regarding teen driver risk, you are not powerless. By understanding the factors that influence the premium—specifically the choice of vehicle and the application of key discounts like the good student discount—you can effectively manage the expense. The investment in higher premiums is a temporary phase that supports your teen’s safety and gradually decreases as they gain experience and responsibility on the road.

Frequently Asked Questions (FAQ)

1. Is it cheaper to insure a teen on my policy or get their own?

It is almost always significantly cheaper to add them to your existing policy. This allows them to benefit from your multi-policy discounts and clean driving record history with the insurer.

2. Does my teen need their own insurance if they have a license but no car?

If your teen has a license and lives with you, they need to be listed on your auto insurance policy. If they occasionally drive your car, they must be covered. If they never drive, you can sign an “exclusion form,” but then they cannot drive any vehicle at all without voiding your coverage.

3. What is the best discount for a teen driver?

The Good Student Discount is typically the most valuable, saving families 10% to 20% on the teen’s portion of the premium. Always provide proof of grades to your insurer.

4. Will my insurance go down when my teen turns 18?

Yes, you will likely see a slight decrease, but the most significant drop usually happens around age 25, provided the driver maintains a clean record. Each year of experience helps lower the rate.

5. Should I buy my teen an old car to save on insurance?

It depends. If you buy an old car worth very little, you can drop comprehensive and collision coverage, saving money. However, if the car is old and lacks modern safety features, or if it is a high-horsepower “muscle car” from the 2000s, it could still be expensive to insure for liability.

Additional Resource

For the most up-to-date statistical data on teen drivers and the risks associated with young drivers, we highly recommend visiting the Centers for Disease Control and Prevention (CDC) – Teen Drivers page. This government resource provides the factual backbone for why insurance rates are structured the way they are.