For many families and individuals considering circumcision, whether for a newborn, a child, or an adult, one of the most pressing questions is about cost. Specifically, you want to know how much financial protection your health insurance provides. The answer, while not simple, becomes clear when you understand how insurance companies categorize and cover this common procedure. This guide will walk you through every factor that influences the final price you pay, empowering you to make informed decisions and avoid unexpected bills.

Circumcision Costs with Insurance

Understanding Circumcision: Medical vs. Ritual

Before diving into costs, it’s crucial to distinguish how the procedure is classified, as this directly impacts insurance coverage.

-

Medical Circumcision: This is performed to treat or prevent specific health conditions. Common medical reasons include recurrent balanitis (inflammation of the foreskin), phimosis (the inability to retract the foreskin), and urinary tract infections. For infants, while less common, a medical necessity might be cited for anatomical abnormalities.

-

Ritual or Elective Circumcision: This is performed for religious, cultural, or personal preference reasons in the absence of a diagnosed medical condition. The most common example is the routine circumcision of a healthy newborn.

Why does this matter? Most insurance plans, including Medicaid in many states, typically cover procedures deemed medically necessary. Elective or ritual procedures are often considered non-essential and may not be covered, leaving the patient responsible for the full cost.

How Much Does Circumcision Cost with Insurance? The Breakdown

The out-of-pocket cost with insurance is rarely a single flat fee. It is a sum of several parts, dictated by your specific plan’s structure. Here’s a realistic breakdown of what you might pay.

Key Cost Components

Your total bill will typically consist of:

-

Surgeon/Facility Fee: The cost for the doctor’s skill and the use of the hospital or outpatient clinic.

-

Anesthesia Fee: Charges for the anesthetic administered.

-

Post-Operative Care: Follow-up visits and any necessary supplies.

With insurance, you pay according to your plan’s rules until you meet your deductible and out-of-pocket maximum.

Estimated Out-of-Pocket Costs Table

The following table illustrates potential cost scenarios based on a hypothetical total procedure cost of $2,500.

| Insurance Plan Scenario | Deductible Status | Co-insurance | Estimated Patient Cost | Notes |

|---|---|---|---|---|

| Plan with Low Deductible (Met) | Deductible already met | 20% | $500 | You pay only the co-insurance. Common in comprehensive plans. |

| Plan with High Deductible (Not Met) | $3,000 deductible not met | 20% (after deductible) | $2,500 | You pay the full billed amount, which applies toward your deductible. |

| Co-pay Plan | N/A | Fixed co-pay | $250 – $500 | Some plans have a set surgical co-pay. Less common for procedures. |

| Elective Procedure | N/A | 0% (not covered) | $1,500 – $3,000+ | Full patient responsibility. Price may be lower as a cash-pay service. |

Note: These are illustrative examples. Your actual costs depend on your insurer’s negotiated rates with your provider.

The Role of Your Deductible, Co-pay, and Co-insurance

-

Deductible: The amount you pay for covered services before your insurance starts to pay. If you haven’t met your deductible, you will likely pay the insurer’s negotiated rate for the entire procedure.

-

Co-pay: A fixed amount you pay for a covered service. For specialist visits, this might be $30-$50, but for a surgical procedure, it could be higher if your plan uses a co-pay structure.

-

Co-insurance: Your share of the costs of a covered service, calculated as a percentage (e.g., 20%) after you’ve paid your deductible.

As one healthcare financial advisor notes:

“The sticker price for a procedure is almost irrelevant. What matters is your plan’s negotiated rate and where you are in your deductible cycle. Always call both your insurer and the provider’s billing department for the most accurate estimate.”

Infant Circumcision vs. Adult Circumcision: Cost Differences

The age of the patient significantly affects the complexity, setting, and thus the cost.

Newborn Circumcision:

-

Typical Setting: Hospital nursery or pediatrician’s office shortly after birth.

-

Procedure: Generally simpler, often without general anesthesia.

-

Cost with Insurance: If covered, parents typically pay their delivery/hospital stay co-pay or co-insurance, which often bundles the newborn’s routine care. If it’s a separate charge and deemed routine (not medical), you may pay 100%.

Adult Circumcision:

-

Typical Setting: Outpatient surgery center or hospital.

-

Procedure: More complex, usually requiring local or general anesthesia.

-

Cost with Insurance: If deemed medically necessary (e.g., for phimosis), your cost is governed by your deductible and co-insurance. You are more likely to have met some of your deductible earlier in the year.

Step-by-Step: How to Verify Your Insurance Coverage

Don’t rely on assumptions. Follow these steps to get a clear financial picture.

-

Review Your Plan Documents: Log into your insurer’s portal and find the Summary of Benefits and Coverage (SBC). Look for terms like “male circumcision,” “routine vs. medical,” and “well-baby care.”

-

Call Your Insurance Provider: Have your plan ID ready. Ask these specific questions:

-

“Does my plan cover circumcision for a newborn as part of routine well-baby care?”

-

“What is the coverage criteria for an adult circumcision deemed medically necessary?”

-

“What is my deductible, and how much have I met this year?”

-

“What is my co-insurance rate for outpatient surgery?”

-

“Do I need a referral or pre-authorization?”

-

“Are the specific hospital/urologist/pediatrician I’m considering in-network?”

-

-

Call the Healthcare Provider’s Billing Department: Ask for the CPT code they will use (common codes are 54150 for infant and 54161 for adult). Then, ask:

-

“What is your cash-pay price for this procedure if insurance doesn’t cover it?”

-

“Can you provide a detailed estimate of all fees (surgeon, facility, anesthesia)?”

-

Important Note for Readers: Always get cost information and pre-authorization confirmations in writing from your insurance company. Verbal quotes are not binding.

What If Insurance Doesn’t Cover It? Exploring Other Options

If you learn the procedure is not covered, all is not lost. You have several paths forward.

-

Negotiate a Cash-Pay Price: Providers often have lower, self-pay rates that bypass the complexity of insurance billing. Don’t hesitate to ask.

-

Payment Plans: Most hospitals and clinics offer interest-free or low-interest payment plans to spread the cost over several months.

-

Healthcare Savings Accounts (HSA/FSA): You can use pre-tax dollars from these accounts to pay for circumcision, even if it’s elective, as it is considered a qualified medical expense by the IRS.

-

Look into Community Health Clinics: Some clinics offer the procedure at a significantly reduced cost on a sliding scale based on income.

Frequently Asked Questions (FAQ)

Q: Do Medicaid and Medicare cover circumcision?

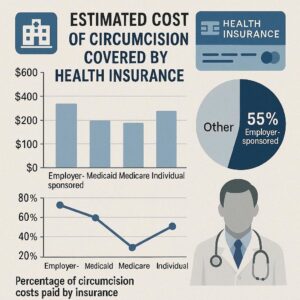

A: Medicaid coverage for routine newborn circumcision varies by state. Some states cover it, others do not. Adult circumcision is covered if medically necessary. Medicare Part B may cover adult circumcision if a doctor certifies it is medically required to treat an illness or injury.

Q: How can I increase the chance of insurance approval for an adult circumcision?

A: Thorough documentation from your doctor is key. They must provide a letter of medical necessity, citing the specific diagnosed condition (like phimosis), history of treatments tried and failed, and how the procedure will resolve the issue.

Q: Are there any hidden costs I should ask about?

A: Yes. Always ask if the estimate includes the anesthesiologist’s fee (they are often separate from the surgeon) and charges for any required pathology if the foreskin is sent to a lab.

Q: Is circumcision typically covered under “preventive care” benefits?

A: No. Under the Affordable Care Act, preventive care is specific to services like immunizations and screenings. Routine circumcision is not classified as preventive care for insurance purposes.

Conclusion

The cost of circumcision with insurance is a variable equation, not a fixed number. It hinges on the procedure’s medical necessity, your specific plan’s deductible and co-insurance structure, and the patient’s age. By proactively verifying your benefits, understanding your plan’s details, and communicating openly with both your insurer and healthcare provider, you can transform a confusing financial question into a manageable, planned expense. The most powerful tool at your disposal is informed inquiry.

Additional Resource:

For a non-profit breakdown of state-by-state Medicaid policies on newborn circumcision, visit the American Academy of Pediatrics Circumcision Policy Resource Page.