If you live in the Bluegrass State—or are planning to move there—you have probably asked yourself, “How much am I going to pay for car insurance?” Whether you are cruising down I-64 in Louisville, navigating the rural roads of Bowling Green, or commuting through the suburbs of Lexington, car insurance is a non-negotiable part of life.

But here is the thing: the “average” number you see online can be misleading. It rarely tells the full story of what you will pay. In this guide, we are going to break down the average car insurance cost in Kentucky with complete transparency. We will look at why rates vary, how your city affects your premium, and most importantly, how you can keep more money in your pocket while staying fully protected.

Let’s get started.

Cost of Car Insurance in Kentucky

What is the Average Car Insurance Cost in Kentucky?

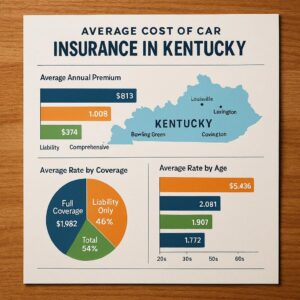

To set the stage, we need to look at the baseline figures. According to recent industry data, the average cost of full coverage car insurance in Kentucky hovers around $1,800 to $2,000 per year. For state-minimum liability coverage, drivers typically pay between $450 and $550 annually.

However, it is vital to understand that Kentucky is unique. It is one of the few states that uses a “choice” no-fault system. This legal framework has a direct impact on your premiums, often making them slightly higher than the national average.

To put this into perspective, here is a quick comparison:

-

National Average (Full Coverage): ~$1,700 per year

-

Kentucky Average (Full Coverage): ~$1,900 per year

-

Kentucky Average (Minimum Coverage): ~$500 per year

Important Note: These are estimates based on a 30-year-old driver with a clean record. If you have a speeding ticket on your record or if you are insuring a teenage driver, these numbers will change significantly.

Why Are Kentucky Rates Higher Than Some Other States?

You might be wondering why your neighbor in Tennessee pays less than you do for the same car. There are a few specific reasons for the average car insurance cost in Kentucky sitting slightly above the national baseline.

1. The “No-Fault” System

Kentucky operates under a “choice” no-fault system. This means that when you purchase a policy, you have the option to choose whether you want to be covered under no-fault rules or traditional tort (fault) rules.

-

How it affects price: Under the no-fault system, your insurance company pays for your medical bills (Personal Injury Protection or PIP) regardless of who caused the accident. Because insurers know they will have to pay these claims quickly, they adjust premiums to cover that risk.

2. Weather and Road Conditions

Kentucky experiences all four seasons, and the weather can be harsh. Heavy spring rains, icy winter roads, and foggy conditions in the Appalachian foothills lead to a higher frequency of accidents compared to states with mild, dry climates.

3. Litigation Costs

Even in a no-fault state, lawsuits happen. Kentucky has a higher-than-average rate of litigation when it comes to injury claims. Insurance companies factor in the cost of defending these lawsuits when they calculate your premium.

Breaking Down Costs by Major City

Where you park your car at night is one of the biggest factors in determining your rate. Insurance companies look at crime rates, population density, and historical claim data for your specific zip code.

Here is a realistic look at the average car insurance cost in Kentucky’s largest cities.

| City | Average Annual Premium (Full Coverage) | Average Monthly Premium |

|---|---|---|

| Louisville | $2,150 | $179 |

| Lexington | $1,950 | $162 |

| Bowling Green | $1,750 | $146 |

| Owensboro | $1,700 | $142 |

| Covington | $2,050 | $171 |

| Richmond | $1,720 | $143 |

| Florence | $1,890 | $158 |

| Hazard | $1,680 | $140 |

Why the Difference?

-

Louisville and Covington see higher rates due to urban congestion and higher rates of vehicle theft and vandalism.

-

Hazard and Bowling Green tend to have lower rates due to lower population density and fewer comprehensive claims (theft, vandalism).

How Age Impacts Your Premium

Age is another massive factor. Insurance is essentially a bet on risk, and statistically, young and inexperienced drivers are more likely to have accidents.

Teen Drivers (16-19)

Adding a teenager to a policy in Kentucky is expensive. Parents should expect the rate to nearly double.

-

Average Cost: Adding a teen driver can increase an annual policy by $2,500 to $3,500.

-

Pro Tip: Ask about Good Student discounts. If your teen maintains a B average or higher, many major insurers will knock a significant percentage off the premium.

Young Adults (20-29)

Rates start to decrease once a driver hits their mid-twenties. However, credit history (where permitted) and renting an apartment can still keep rates moderately high.

-

Average Cost (25-year-old): Around $1,800 per year.

Middle-Aged Adults (30-50)

This is the “sweet spot” for insurance. Insurers view this demographic as the most stable and least likely to file a claim.

-

Average Cost: Between $1,600 and $1,750 per year.

Seniors (65+)

Rates often tick back up slightly for seniors. This is not ageism; it is based on data showing that reaction times can slow with age, and the severity of medical injuries in accidents tends to be higher.

-

Average Cost: Between $1,700 and $1,900 per year.

A Look at Kentucky’s Major Insurance Providers

Not all insurance companies are created equal, and they don’t all charge the same rates. In fact, you could save hundreds of dollars just by shopping around. Each company has a different “appetite” for risk. Some love to insure drivers with perfect records; others are more forgiving but charge a baseline premium to cover that risk.

Here is a comparison of the average annual rates for major insurers operating in Kentucky.

| Insurance Company | Avg. Annual Rate (Full Coverage) | Best For… |

|---|---|---|

| State Farm | $1,750 | Drivers with clean records / Great local agents |

| GEICO | $1,680 | Budget-conscious / Military families |

| Progressive | $1,890 | High-risk drivers / SR-22 filings |

| Allstate | $2,100 | Bundling home & auto / New car replacement |

| Kentucky Farm Bureau | $1,600 | Rural drivers / Long-term relationship discounts |

| USAA | $1,550 | Military members and their families (Eligibility required) |

Reader Note: The table above is a guideline. Your actual rate will depend on your specific address, driving history, and the vehicle you drive. Always get personalized quotes.

Minimum Coverage Requirements in Kentucky

If you own and operate a vehicle in Kentucky, you must carry a minimum amount of liability insurance. Driving without it is illegal and financially dangerous.

Kentucky law requires the following limits:

-

Bodily Injury Liability: $25,000 per person / $50,000 per accident.

-

Property Damage Liability: $25,000 per accident.

-

Personal Injury Protection (PIP): $10,000 (This is mandatory under the no-fault system).

Why You Should Buy More Than the Minimum

While the minimum coverage is the cheapest way to get a license plate, it is rarely the smartest financial decision. If you cause a serious accident involving another vehicle, the $25,000 property damage limit might not cover the cost of a new Tesla or even a fully-loaded pickup truck. If the damages exceed your limit, you can be sued personally for the difference.

How to Lower Your Car Insurance Costs

Feeling like you are paying too much? You are not alone. Fortunately, there are legitimate ways to lower the average car insurance cost in Kentucky for your specific situation.

1. Bundle Your Policies

This is the easiest way to save. If you own a home or rent an apartment, getting your auto and home/renters insurance from the same company can save you up to 25% on both policies.

2. Ask About Discounts

Insurance companies have dozens of discounts, but they won’t always apply them unless you ask. Common discounts include:

-

Multi-car discount: Insuring two or more vehicles.

-

Anti-theft discount: For cars with alarms or tracking systems.

-

Defensive driving course: Especially beneficial for seniors.

-

Paid-in-full discount: Paying your six-month premium upfront rather than monthly.

3. Improve Your Credit Score

In Kentucky, insurance companies are allowed to use credit-based insurance scores to determine your rate. Generally, drivers with good credit pay significantly less than those with poor credit. Paying down debt and ensuring your bills are paid on time can lead to lower premiums when your policy renews.

4. Drop Comprehensive and Collision on Older Cars

If you are driving a vehicle that is worth less than $4,000, it might be time to drop the physical damage coverage. If you get into an accident, the insurance company will only pay out the actual cash value of the car. If that value is low, it might not be worth paying the premium.

Understanding Kentucky’s “Choice” No-Fault System

We touched on this earlier, but it deserves a deeper look because it directly affects the average car insurance cost in Kentucky and how you get paid after an accident.

When you buy a policy in Kentucky, you have two choices regarding how you are covered:

Option 1: No-Fault (The Default)

-

You carry Personal Injury Protection (PIP) which pays your medical bills immediately, no matter who caused the accident.

-

You give up your right to sue the other driver for “pain and suffering” unless your injuries are severe (defined by law as permanent, serious, or disfiguring).

-

Result: Faster payment for medical bills, but limited ability to sue.

Option 2: Tort (Fault)

-

You reject the no-fault limits in writing.

-

You do not have to carry PIP (though it is still recommended).

-

You retain the full right to sue the at-fault driver for pain and suffering, even in minor accidents.

-

Result: More legal rights, but you must wait for the at-fault driver’s insurance to pay, which can take time.

Important Note: If you choose the Tort option, you are still subject to Kentucky’s laws regarding lawsuits. Make sure you understand the legal implications before signing a waiver.

Frequently Asked Questions (FAQ)

1. Is Kentucky a no-fault state for car insurance?

Yes, Kentucky is a “choice” no-fault state. This means you can choose whether to be covered under no-fault rules (where your insurance pays your medical bills) or tort rules (where you retain the right to sue). Unless you sign a waiver rejecting it, you are covered under the no-fault system.

2. How much is car insurance per month in Kentucky?

The average monthly cost for full coverage car insurance in Kentucky is approximately $150 to $160. However, this varies widely. Drivers with minimum coverage might pay as little as $40 per month, while high-risk drivers could pay over $200 per month.

3. Why is my car insurance so high in Kentucky?

Your rates might be high due to a combination of factors: living in a high-traffic area like Louisville, having a recent accident or ticket, having poor credit, or choosing high coverage limits. Additionally, Kentucky’s no-fault laws require insurers to include PIP coverage, which adds to the premium.

4. Does my credit score affect my car insurance rate in Kentucky?

Yes, in most cases. Insurance companies in Kentucky are permitted to use your credit history to calculate your premium. Statistically, drivers with better credit file fewer claims, so they are rewarded with lower rates.

5. What is the cheapest car insurance in Kentucky?

Based on market data, USAA tends to be the cheapest for military families, while GEICO and Kentucky Farm Bureau often offer the most competitive rates for the general public. However, the “cheapest” company varies by individual driver profile.

Additional Resource: Do Your Research

To ensure you are getting the best deal, it is wise to consult independent resources. The Kentucky Department of Insurance provides consumer guidance and can help you understand your rights as a policyholder. You can visit their official website for more information on company complaints and financial ratings.

Conclusion

Understanding the average car insurance cost in Kentucky is the first step toward financial empowerment. While the state average hovers around $1,900 per year for full coverage, your personal rate is a unique combination of your location, age, driving history, and the choices you make regarding coverage. By shopping around, asking for discounts, and understanding Kentucky’s unique no-fault system, you can find a policy that protects you without breaking the bank.

Final Summary

In Kentucky, the average driver pays about $1,900 annually for full coverage, though rates vary significantly by city and age. The state’s “choice” no-fault system requires Personal Injury Protection, which impacts premiums. To get the best rate, compare quotes from multiple insurers and always ask about available discounts.