Congratulations on your new car! Whether you’re cruising down A1A or navigating I-95, that new vehicle is a significant investment. But in the excitement of driving off the lot, many Florida drivers overlook a critical financial safeguard: Guaranteed Asset Protection (GAP) insurance. If your new car is totaled or stolen, your standard auto insurance payout might not cover what you still owe on your loan or lease. That’s where Gap insurance comes in. This comprehensive guide will break down everything you need to know about Gap insurance Florida cost, helping you make an informed decision to protect your finances.

Gap Insurance Cost in Florida

What is Gap Insurance and How Does It Work in Florida?

Gap insurance is a specialized type of coverage designed to bridge the “gap” between the actual cash value (ACV) of your vehicle at the time of a total loss and the remaining balance on your auto loan or lease. In Florida, where new car purchases and leases are common, this coverage can be a financial lifesaver.

Here’s a typical scenario: You buy a new SUV in Tampa for $35,000 with a small down payment. A year later, after an accident, it’s declared a total loss. Your standard auto insurer determines the SUV’s current market value is only $28,000. However, you still owe $32,000 on your loan. Without Gap insurance, you would be responsible for paying the $4,000 difference out-of-pocket—even though you no longer have the car.

“Gap insurance isn’t for your car; it’s for your loan. It’s the buffer between depreciation and debt, a crucial layer of protection for any financed vehicle in its early years,” explains a veteran Florida insurance advisor.

The Florida Context: Why It Matters Here

Florida’s high rate of new vehicle sales, combined with common financing terms of 72+ months, creates a perfect environment where borrowers can be “upside-down” on their loans (owing more than the car is worth) for several years. Add to that the risk of hurricanes, flooding, and high traffic accident rates in cities like Miami and Orlando, and the need for Gap coverage becomes even more apparent.

Key Factors That Influence Your Gap Insurance Premium in Florida

The cost of Gap insurance in Florida is not a one-size-fits-all figure. Several variables determine your specific premium:

-

Vehicle Type and Value: New cars depreciate faster, especially luxury brands or models with high initial MSRPs. This typically leads to a higher Gap insurance cost.

-

Loan Terms: The size of your down payment, loan amount, interest rate, and loan term (e.g., 60 vs. 84 months) directly impact the risk and potential size of the gap.

-

Your Chosen Provider: Costs vary significantly between buying from your car dealer, your primary auto insurer, or a standalone specialty insurer.

-

Your Driving Location: While less impactful than other factors, your specific ZIP code in Florida can influence cost due to localized risk assessments.

-

Coverage Amount and Deductibles: Some policies offer variations in terms of what they cover (e.g., including your primary insurance deductible).

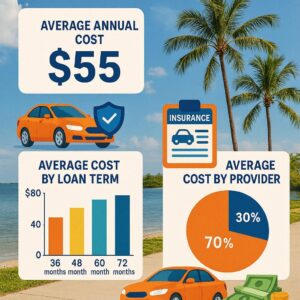

Breaking Down the Cost: Sample Gap Insurance Premiums in Florida

To give you a realistic idea of pricing, here are sample annual cost ranges for a Gap insurance policy in Florida for a typical new vehicle purchase. These are illustrative estimates based on market research.

Comparative Cost Table: Gap Insurance Providers in Florida

| Provider Type | Average Annual Cost Range | Pros | Cons |

|---|---|---|---|

| Through Your Auto Insurer | $20 – $40 per year (added to premium) | Convenient, often cheapest, integrated billing. | Requires a full coverage policy with that insurer. |

| Through Your Car Dealership | $400 – $800 as a one-time fee (often financed) | Extremely convenient at point of sale. | Almost always the most expensive option; cost is added to loan and accrues interest. |

| Standalone Specialty Insurer | $200 – $400 as a one-time flat fee | Can be more competitive than dealerships; portable. | Requires separate research and purchase. |

Cost Analysis by Vehicle Loan Scenario

The following table illustrates how your financial decisions affect the potential gap and the value of the coverage.

| Vehicle Purchase Price | Down Payment | Loan Term | Amount Owed After 1 Year | Likely ACV After 1 Year | Potential Gap | Gap Insurance Value |

|---|---|---|---|---|---|---|

| $30,000 | $3,000 (10%) | 72 months | ~$27,500 | ~$24,000 | $3,500 | High |

| $30,000 | $6,000 (20%) | 60 months | ~$23,500 | ~$24,500 | -$1,000 (No Gap) | Low/Unnecessary |

| $45,000 | $4,500 (10%) | 84 months | ~$42,000 | ~$36,000 | $6,000 | Very High |

Important Note: These are simplified estimates. Depreciation rates vary by make and model. Always calculate your specific situation.

Where and How to Buy Gap Insurance in Florida: A Strategic Guide

1. From Your Auto Insurance Company (Often the Best Value)

Most major insurers in Florida (like State Farm, GEICO, Progressive, Allstate) offer a “loan/lease payoff” endorsement. This is generally the most cost-effective way to purchase Gap coverage.

-

Process: Simply call your agent or add it through your online portal. It becomes part of your regular bill.

-

Tip: Always get a quote from your insurer before visiting the dealership.

2. At the Car Dealership (Convenient but Costly)

The finance manager will offer you Gap insurance when you sign your paperwork.

-

Process: The cost is rolled into your total loan amount.

-

Crucial Tip: You can (and should) politely decline the dealer’s offer. You are under no obligation to buy it from them. Say, “I will be arranging Gap coverage separately with my insurer.” This alone can save you hundreds.

3. Through a Bank, Credit Union, or Specialty Provider

Some lenders and online specialty companies offer standalone Gap policies.

-

Process: Requires separate application and payment.

-

Tip: Compare their one-time flat fee to the annualized cost from your auto insurer over your expected loan term.

Is Gap Insurance Mandatory in Florida?

No, Florida law does not require drivers to purchase Gap insurance. However, your lender or leasing company may require it as a condition of your loan or lease agreement. This is especially common for leases and loans with low down payments. Always check your contract.

When Do You Absolutely Need Gap Insurance? A Florida Driver’s Checklist

You are a strong candidate for Gap insurance if:

-

You made a down payment of less than 20%.

-

Your loan term is 60 months or longer.

-

You leased your vehicle (highly recommended for leases).

-

You financed a vehicle that depreciates faster than average (e.g., many luxury sedans).

-

You rolled negative equity from a previous loan into your new one.

Steps to Calculate Your Personal Gap and Determine Need

-

Find Your Loan Payoff Amount: Check your latest statement or lender’s portal.

-

Estimate Your Car’s Actual Cash Value: Use tools like Kelley Blue Book (KBB) or NADA Guides. Be honest about condition and mileage.

-

Do the Math: Loan Payoff – Estimated ACV = Potential Gap.

-

Evaluate: If the number is significant ($2,000+), Gap coverage is likely a wise purchase for peace of mind.

Maximizing Value: Smart Tips to Save on Gap Insurance in Florida

-

Shop Your Auto Insurance First: This is your #1 money-saving strategy.

-

Consider a Larger Down Payment: Putting down 20% or more can often eliminate the gap from day one.

-

Choose a Shorter Loan Term: 36 or 48-month loans build equity faster and reduce the gap period.

-

Negotiate the Dealer’s Price: If you prefer the dealer’s convenience, the fee is often negotiable. Don’t accept the first quote.

-

Review Annually: As your loan balance decreases and your car depreciates, the gap shrinks. You may be able to drop the coverage after 2-3 years.

Frequently Asked Questions (FAQ)

Q: How long do I need to keep Gap insurance?

A: Typically, you only need it for the first 2-3 years of your loan or for the entire lease term. Once your loan balance falls below your car’s market value, you can cancel it.

Q: Can I cancel dealer-purchased Gap insurance?

A: Yes, you can usually cancel it and receive a pro-rated refund. The refund will be sent directly to your lender to reduce your principal balance, not to you. Contact your lender’s financial office for the specific process.

Q: Does Gap insurance cover my deductible?

A: Standard Gap insurance does not. However, some policies, often called “Gap with Deductible Coverage” or “Vehicle Replacement Assistance,” may include this. Confirm with your provider.

Q: Is Gap insurance the same as “new car replacement” coverage?

A: No. New car replacement (offered by some auto insurers) replaces your totaled car with a brand-new model of the same kind. Gap insurance only covers the financial shortfall on your loan. They are different but sometimes complementary coverages.

Conclusion

Understanding Gap insurance Florida cost is key to making a smart financial decision as a car owner. By recognizing that the cheapest option is usually through your existing auto insurer, avoiding the inflated cost at the dealership, and carefully assessing your personal loan-to-value risk, you can secure essential protection without overpaying. Protect your investment, safeguard your finances, and drive Florida’s roads with greater confidence.