Buying a home is one of the biggest investments you will ever make. Protecting that investment is not just smart; it is essential. But if you are shopping for insurance, you have likely run into a wall of jargon and policy numbers. Two of the most common you will see are HO-3 and HO-6.

If you are currently trying to figure out your budget, the first question on your mind is probably about the HO-3 vs HO-6 insurance cost.

It is a logical question. However, the answer is not as simple as “Policy A is cheaper than Policy B.” The cost difference depends entirely on what you are insuring. You cannot compare the price of insuring a detached house to the price of insuring a condo unit inside a larger building—it would be like comparing the cost of insuring a car to the cost of insuring a motorcycle.

In this guide, we will break down everything you need to know. We will look at what these policies cover, why their costs differ, and how you can get the best rate for your specific situation. By the end, you will have a clear roadmap for your next conversation with an insurance agent.

Important Note: Insurance regulations and average costs vary significantly depending on where you live. The prices mentioned in this article are estimates based on national averages and should be used as a conceptual guide, not as a formal quote.

What Are HO-3 and HO-6 Policies? (The Basics)

Before we talk money, we have to talk about what these policies actually do. Think of insurance policy forms (HO-3, HO-6, etc.) as recipes. They tell the insurance company exactly what ingredients (coverage) go into the cake (your policy).

The HO-3 Policy: The Standard for Homeowners

If you own a single-family home, a townhouse, or a duplex, you will almost always be shopping for an HO-3 policy. It is the most common homeowners insurance policy in the United States.

-

Who it’s for: Homeowners who own the structure of the house and the land it sits on.

-

What it covers (Dwelling): This is the most important part. The HO-3 uses what is called “open perils” coverage for the structure of your home. That sounds technical, but it is actually a very good thing. It means your house is covered for everything unless it is specifically listed as an exclusion in the policy. Common exclusions are things like floods, earthquakes, and normal wear and tear.

-

What it covers (Belongings): Your furniture, clothes, and electronics are covered under “named perils.” This means they are only protected against events specifically listed in the policy, like fire, theft, or windstorms.

-

Other coverages: It also includes liability protection (if someone gets hurt on your property) and coverage for additional living expenses if your home becomes uninhabitable due to a covered claim.

Think of the HO-3 as a comprehensive shield for the entire property.

The HO-6 Policy: Designed for Condo Owners

If you live in a condominium or a co-op, you need an HO-6 policy, often called “walls-in” or “unit-owners” insurance. It works very differently because you do not own the entire building.

-

Who it’s for: Condo and co-op unit owners.

-

The Master Policy: Your condo association has a master insurance policy that covers the building’s exterior, common areas (like lobbies and hallways), and the basic structure of your unit (the “bare walls”). The HO-6 policy is designed to fill in the gaps that the master policy leaves behind.

-

What it covers (Dwelling): The HO-6 covers the interior of your unit. This includes things like interior drywall, flooring, cabinets, built-in appliances, and improvements you have made (like that nice backsplash you installed).

-

What it covers (Belongings): Just like the HO-3, it covers your personal property against named perils.

-

Loss Assessments: This is a unique and vital feature of the HO-6. If a fire damages the building’s roof and the cost exceeds the master policy’s limit, the association might bill each owner (an “assessment”) for their share. Your HO-6 policy often includes coverage to pay that bill for you.

-

Other coverages: It also includes liability coverage for incidents that happen inside your unit.

Think of the HO-6 as a protective bubble inside a larger building that is already partially insured.

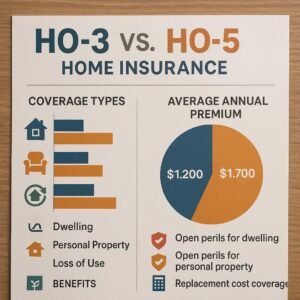

HO-3 vs HO-6 Insurance Cost: Breaking Down the Price Difference

Now, let’s get to the heart of the matter. If you were to look at the average annual premium for an HO-3 policy versus an HO-6 policy, you would see a significant difference.

According to recent industry data:

-

Average HO-3 Cost: Around $1,200 to $1,500 per year for a standard single-family home.

-

Average HO-6 Cost: Around $400 to $600 per year for a standard condo unit.

So, the HO-3 vs HO-6 insurance cost comparison shows that HO-3 policies are generally much more expensive. But why?

It is not because insurance companies like to charge homeowners more. It is because the level of financial risk is completely different.

| Feature | HO-3 (Homeowners) | HO-6 (Condo) |

|---|---|---|

| Primary Structure Insured | The entire house (roof, walls, foundation). | Interior fixtures, upgrades, and personal belongings. |

| Replacement Cost Value | High ($250,000 – $500,000+). | Low to Medium ($20,000 – $60,000 typically). |

| External Risk | Fully exposed to wind, hail, fire, and theft. | Building exterior is covered by the master policy. |

| Liability Exposure | Higher (property, yard, fences). | Lower (confined to the unit). |

| Average Annual Premium | Higher ($1,200+) | Lower ($500) |

Why the HO-3 Costs More

-

You are Insuring a Building: When you buy an HO-3, you are taking on the financial responsibility for the entire structure. If a tree falls on the roof, your policy pays to fix it (minus your deductible). If a fire destroys the house, your policy pays to rebuild it. That is a massive potential payout for the insurance company, so the premium reflects that risk.

-

External Exposures: A detached home is fully exposed to the elements. Wind, hail, falling trees, and vandalism are all direct threats to your property.

-

Larger Liability Risk: You have a yard, a driveway, and a sidewalk. There are more opportunities for someone to get hurt on your property, which increases your liability risk.

Why the HO-6 Costs Less

-

Shared Risk: The biggest risks are covered by the condo association’s master policy. If the roof leaks or the exterior walls are damaged, the association pays for it (using money from all the unit owners’ dues).

-

Smaller Coverage Amounts: You are insuring the “stuff” inside your walls. Unless you have a penthouse with marble floors, the total value of your interior structure and belongings is usually much lower than the value of an entire house.

-

Limited External Exposure: Your liability is mostly confined to what happens inside your four walls.

5 Key Factors That Influence Your Specific Rate

While averages are helpful, your actual premium will be determined by a mix of personal and property-specific factors. Here is what moves the needle on your final price.

1. Location, Location, Location

This is the biggest factor for both policies.

-

Catastrophe Zones: If you live on the coast in Florida (hurricanes), in Kansas (tornadoes), or near a wildfire zone in California, your HO-3 rates will be significantly higher. For an HO-6, your master policy rates will go up (raising your HOA fees), but your individual policy might also increase due to higher risk of claims.

-

Crime Rates: Homes in areas with higher burglary rates will cost more to insure.

-

Local Fire Protection: If your home is miles from the nearest fire hydrant or fire station, your rates will be higher. Insurance companies love to see a good fire protection class rating for your area.

2. The Dwelling Coverage Amount

This is the bedrock of your premium.

-

For HO-3: This is the estimated cost to rebuild your home from the ground up, not its market price. A house in a high-cost construction area will have a higher dwelling limit and a higher premium.

-

For HO-6: This is the amount of insurance on the interior of your unit. If you have high-end custom kitchens and bathrooms, you need a higher coverage limit, which will increase your cost.

3. Your Deductible

This is the amount you pay out of pocket before insurance kicks in.

-

A standard deductible is often $500, $1,000, or $2,500.

-

The Trade-Off: Choosing a higher deductible (e.g., $2,500) will usually lower your annual premium. However, you need to make sure you have that cash available if you have a claim. It is a smart way to save money if you are a safe, claim-free homeowner.

4. Your Claims History

Insurance is a bet on the future based on the past.

-

If you (or the previous owner of your home) have filed multiple claims in the last few years, you are statistically more likely to file another one. Insurers will see you as a higher risk and charge you more.

-

Even for condo owners, a history of claims (like a water leak from your unit) can follow you and increase your HO-6 premium.

5. Discounts You Qualify For

This is where you can fight back against high prices. Always ask your agent about discounts.

Common Discounts for HO-3 and HO-6:

-

Bundling: Combining your home and auto insurance with the same company is almost always the easiest way to save 10-25%.

-

Claims-Free: If you haven’t filed a claim in 3-5 years, many companies offer a discount.

-

Security Systems: Monitored burglar alarms, fire alarms, and sprinkler systems can lower your rate.

-

Newer Home/Updates: Newer roofs, updated electrical wiring, and new plumbing are less likely to cause a claim, so you get a better rate.

HO-3 vs HO-6 Insurance Cost

The Hidden Costs: What Your Premium Doesn’t Show You

When looking at the HO-3 vs HO-6 insurance cost, you must look beyond the premium. The true cost of ownership includes the financial gaps you might be responsible for.

The HO-3 “Ordinance or Law” Gap

Let’s say your 100-year-old home is damaged by a fire. You have an HO-3 policy with enough dwelling coverage to rebuild it. However, modern building codes now require fire sprinklers and different electrical wiring. Your policy might pay to rebuild the house to its original state, but not to bring it up to the new code. This can cost you tens of thousands of dollars out of pocket.

-

The Fix: You need to add Ordinance or Law coverage (also called Building Code coverage) to your HO-3 policy. It costs a little more, but it ensures your home is rebuilt to current standards.

The HO-6 “Master Policy” Gap

This is the biggest trap for condo owners. You cannot buy an HO-6 policy without first reading your association’s master policy. Why? Because you need to know what the master policy doesn’t cover.

Master policies generally fall into two categories:

-

“Bare Walls” Coverage: The association only covers the bare studs, concrete, and exterior. You are responsible for everything inside, including drywall, wiring, plumbing, and fixtures.

-

“All-In” Coverage: The association covers the structure as originally built, including drywall and basic fixtures. You are only responsible for improvements (upgraded floors, cabinets) and personal belongings.

If you have a “Bare Walls” master policy, you need a much higher amount of dwelling coverage on your HO-6 than if you have an “All-In” policy. Buying the wrong amount is a financial disaster waiting to happen.

Important Note: Request a copy of the master policy or a “certificate of insurance” from your condo association before you finalize your HO-6 policy. Show it to your insurance agent so they can help you choose the correct coverage limits.

How to Get the Best Rate on Your HO-3 or HO-6 Policy

Armed with all this information, here is your action plan to get the best value for your money.

For the HO-3 Shopper:

-

Shop Around, but Compare Apples to Apples: Get quotes from at least three different insurers. When you do, make sure the coverage limits and deductibles are the same so you are comparing price accurately.

-

Maximize Your Deductible: If you have an emergency fund, raise your deductible to the highest level you can comfortably afford. This can slash your premium by up to 25%.

-

Ask About Bundling: Get a quote for bundling your home and auto insurance immediately. It is almost always cheaper than having them separate.

-

Invest in Prevention: Install storm shutters, a new roof (if needed), and a security system. These are upfront costs that pay for themselves in lower premiums over time.

-

Review Your Policy Annually: Don’t just auto-pay the renewal. Call your agent once a year and ask, “Are there any new discounts I qualify for? Is this still the best rate you can offer me?”

For the HO-6 Shopper:

-

Master Policy First: Before you do anything, get the details of the association’s master policy. This is non-negotiable.

-

Calculate Your “Stuff” and “Updates”: Take a home inventory. How much would it cost to replace all your furniture and clothes? How much did you spend on that kitchen renovation? That number is your starting point for coverage.

-

Don’t Skimp on Loss Assessment: This coverage is usually cheap for the amount of protection it offers. A $1,000 or $2,000 limit is common, but you can often increase it for a small fee. If your building has a major claim, this coverage is a lifesaver.

-

Bundle if You Can: Even though your HO-6 is cheaper, bundling it with your auto insurance is still a fantastic way to save on both policies.

Additional Resources

Navigating the world of insurance can be tough, but you don’t have to do it alone.

-

Your State’s Department of Insurance: This is a free resource. Most state websites offer consumer guides to compare average rates from different insurers in your area.

-

Trusted Choice (Independent Agents): Website: www.trustedchoice.com. This tool helps you find local independent agents who can shop multiple insurance companies to find you the best coverage and price.

Frequently Asked Questions (FAQ)

1. Can I use an HO-3 policy for my condo?

Generally, no. An HO-3 is designed for a dwelling you own exclusively. It would duplicate coverage with the association’s master policy and likely wouldn’t provide the specific “loss assessment” coverage you need. You need an HO-6.

2. I own a townhouse. Do I need HO-3 or HO-6?

It depends. If you own the land and the structure from the ground up, including the roof and exterior walls, you likely need an HO-3. However, if your townhouse is part of a planned community where the HOA is responsible for the exterior and common areas (like a condo), you might need an HO-6. Always check your HOA agreement.

3. What is the most common claim for HO-3 and HO-6 policies?

For both, water damage is the king of claims. For HO-3, this often comes from burst pipes or weather-related issues. For HO-6, it is frequently from internal plumbing failures, like a washing machine hose bursting or a leaky faucet.

4. Is the “dwelling” coverage amount on my HO-6 the same as my home’s market value?

No. It is the cost to rebuild the interior of your unit, which is almost always much lower than the market value (which includes location, demand, etc.).

5. Will my HO-6 premium go up if the building has a claim?

Potentially, yes. If the building has multiple claims, the association’s master policy premiums will rise, and those costs are often passed down to you via increased HOA fees. However, a claim on the master policy generally won’t go on your personal claims history unless it originated in your unit (e.g., you caused a leak that damaged the units below you).

Conclusion

When comparing HO-3 vs HO-6 insurance cost, remember you are looking at two very different products designed for two very different living situations. The HO-3 is a comprehensive, all-encompassing policy for a standalone home, and its higher cost reflects the full responsibility of protecting an entire structure. The HO-6 is a targeted, gap-filling policy for condo owners, and its lower cost reflects the shared risk model of community living. The key to getting the best value is not just finding the cheapest premium, but ensuring you have the right coverage for your specific type of home and risk exposure.