You wake up on a Tuesday morning, walk downstairs to grab laundry, and splash. Your feet are wet. Your basement has turned into an indoor swimming pool. The boxes of holiday decorations float lazily past your furnace. Your stomach sinks.

The good news? You have insurance. The challenging news? Filing a basement flood insurance claim is rarely as simple as calling your agent and receiving a check.

Basements are tricky spaces. Most standard home insurance policies treat them differently than the rest of your house. And flood insurance? That is a completely separate conversation.

But do not panic. Thousands of homeowners navigate this process every year. You can too. This guide walks you through every single step, from the moment you see water to the day you cash your settlement check. We focus on realistic outcomes, honest advice, and practical actions you can take today.

Let us get your basement—and your peace of mind—back to dry ground.

Understanding Your Coverage: The First (and Most Important) Step

Before you file anything, you need to know what you are working with. Many homeowners assume they have full coverage for basement flooding. Many are wrong. This is not said to scare you. It is said to save you time and frustration.

The Big Distinction: Flood vs. Water Damage

Insurance companies make a sharp difference between two things that look exactly the same: water on your floor.

| Type of Water Event | Typically Covered By | Typical Basement Coverage |

|---|---|---|

| Burst pipe (sudden, accidental) | Standard homeowners insurance | Often yes (water removal, drying, some repairs) |

| Sewer backup (from city main or clog) | Homeowners + Sewer backup endorsement | Only if you added this specific coverage |

| Groundwater seepage through walls/floors | No standard policy | Almost never covered |

| Rising river or heavy rain flood | National Flood Insurance Program (NFIP) or private flood insurance | Limited coverage for specific items (varies by plan) |

| Sump pump failure | Homeowners + Sump pump endorsement | Only if you added this rider |

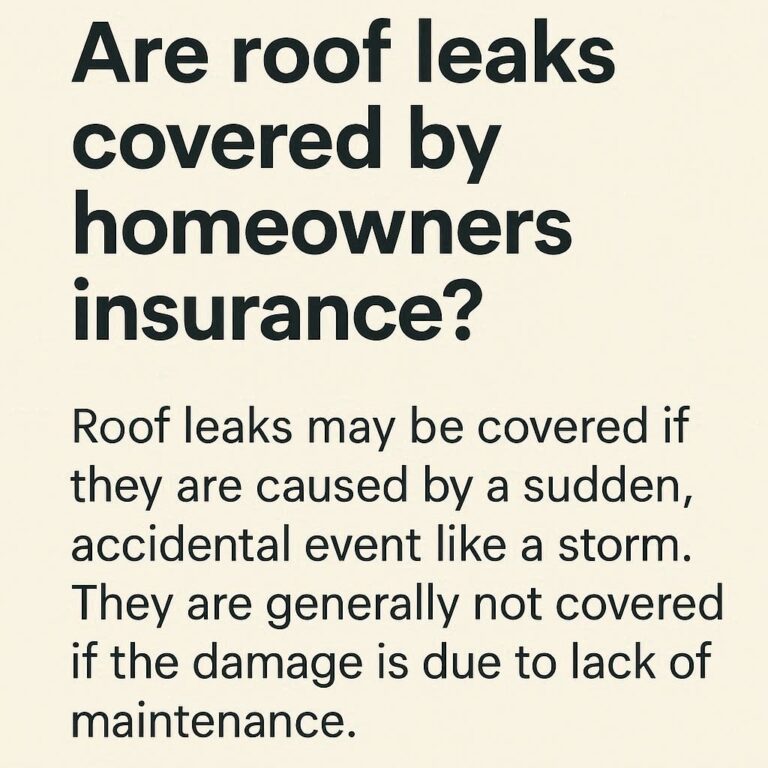

Let us repeat that because it is critical: Standard homeowners insurance rarely covers flooding from outside sources. Groundwater, heavy rain seeping in, or rising rivers are not covered under a typical HO-3 policy.

If your basement flooded because a pipe froze and burst, call your home insurer. If your basement flooded because a storm dumped six inches of rain in two hours and water pushed through your foundation, you need flood insurance.

What Does Flood Insurance Actually Cover in a Basement?

This is where many homeowners get frustrated. The National Flood Insurance Program (NFIP) has very specific rules about basements. Even with a separate flood policy, do not expect a blank check.

Under an NFIP policy, a basement is defined as any area of a building with a floor that is below ground level on all sides. For that space, flood insurance covers:

- Structural elements: Foundation walls, stairways, staircases, elevators, and dumbwaiters.

- Essential equipment: Sump pumps, well-water tanks, solar energy equipment, fuel tanks, and furnaces (including the motor).

- Permanently installed items: Central air conditioning units, electrical junction boxes, circuit breaker boxes, and utility pumps.

- Crawlspace cleanup: Reasonable costs to remove debris and clean the space.

Now here is what flood insurance does not cover in a basement:

- Personal belongings: Furniture, rugs, sofas, mattresses, clothing, electronics, artwork, books, or any movable possession.

- Finished walls and floors: Drywall, paneling, tile, hardwood flooring, carpet, or any interior finishing materials below the lowest elevated floor.

- Wall coverings: Paint, wallpaper, or any decorative treatments.

- Appliances (non-essential): Washers, dryers, refrigerators, freezers, or portable dishwashers.

- Improvements: Built-in bookcases, bars, or entertainment centers.

Read that list again slowly. Yes, that means if your finished basement has a beautiful carpet, leather sofa, 65-inch TV, and a home theater system, a standard NFIP flood policy will pay zero dollars for those items. Private flood insurance may offer more generous terms, but you must read your specific policy.

A Note on Sewer Backup

Many basement floods involve sewer backup. Dirty water pushes up through floor drains or toilets. This is separate from both flood and standard home insurance. Most insurers offer a sewer backup endorsement for an extra 50to250 per year. Without it, you pay for everything out of pocket. If you have this coverage, your basement flood insurance claim will look different. You will file through your home insurer, not FEMA.

Step-by-Step: How to File a Basement Flood Insurance Claim

Let us assume the worst has happened. Water is in your basement. You have confirmed you have either flood insurance, sewer backup coverage, or burst pipe coverage. Now what?

Follow these steps in order. Do not skip any. The order matters more than you think.

Step 1: Stop the Water (If Safe)

Your first job is safety. Do not walk through standing water if electricity could be live. Do not enter water that smells like sewage or chemicals.

If the source is a burst pipe, turn off your main water valve immediately. If the source is heavy rain, you can try to stop more water from entering with sandbags or plastic sheeting over window wells. If the source is sewer backup, stop running any water in the house. No washing machines, dishwashers, or showers dumping water into the system.

Safety note: If you smell gas or see downed power lines near your home, leave immediately and call emergency services. No insurance claim is worth your health.

Step 2: Document Everything Before You Clean

This is the most important step for a successful basement flood insurance claim. Grab your phone and become a documentarian.

Photo and video checklist:

- Wide shots of every basement area showing water depth and spread.

- Close-ups of the water line on walls, appliances, and support columns.

- Photos of damaged items before you move them (furniture, boxes, rugs).

- Photos of the source of water (cracked foundation, backed-up drain, burst pipe).

- Video walking slowly through the space with verbal commentary. Say dates, times, and what the viewer is seeing.

Written inventory:

Open a note on your phone or grab a paper pad. List every damaged item. Include:

- Item name and description

- Approximate age

- Original purchase price (if known)

- Estimated current value

- Serial numbers for electronics and appliances

Do not throw anything away yet. Do not start demolition. Do not cut soggy drywall. Do not drag soaked carpet to the curb. The insurance adjuster needs to see the damage in its original state.

Step 3: Call Your Insurance Company

Call the correct insurer. If the water came from outside (flood), call your flood insurance provider (NFIP or private). If it came from a burst pipe or sewer backup, call your homeowners insurance company.

What to have ready before you call:

- Your policy number

- Date and time the flood started (estimate if unsure)

- Cause of the water (heavy rain, pipe break, sewer backup)

- Estimated water depth

- Your contact information and whether you can stay in the home

- Temporary repairs you have already made (turning off water, placing tarps)

Be calm. Be factual. Do not exaggerate. Do not say “everything is destroyed” unless it truly is. The representative will open a claim and give you a claim number. Write this number down. You will use it constantly.

Ask these three questions during your call:

- How soon will an adjuster contact me?

- Do I need to get repair estimates before the adjuster visits?

- Is there a specific water mitigation company you recommend?

Step 4: Mitigate Further Damage (But Do Not Repair)

Your policy requires you to prevent additional damage. That means you can and should:

- Remove standing water with a pump or wet/dry vacuum (take photos of water depth first).

- Move undamaged items to higher ground (basement stairs, garage, first floor).

- Set up fans, dehumidifiers, and open windows to circulate air.

- Place aluminum foil under furniture legs to prevent staining on wet carpets.

You should not:

- Throw away damaged items.

- Remove drywall or flooring.

- Make permanent structural repairs.

- Sign any contract with a contractor before the adjuster visits.

Keep receipts for everything you spend during mitigation. Pump rentals, fans, dehumidifiers, extension cords, even trash bags. Your policy may reimburse reasonable mitigation costs.

Step 5: Meet the Insurance Adjuster

The adjuster will call to schedule an in-person visit. Be home for this. Do not let them inspect alone. You are there to tell the story of your basement flood.

Before the adjuster arrives:

- Have your documentation ready (photos, videos, inventory lists).

- Gather receipts for any temporary repairs or equipment rentals.

- Prepare a folder of your policy documents.

- Write down questions you want to ask.

During the inspection:

Walk the adjuster through the basement exactly as you documented it. Point out the high-water mark on walls. Show them the damaged items. Mention hidden damage you suspect (water inside walls, under flooring). Be polite but thorough. Do not be afraid to ask:

- “How did you determine that value?”

- “Is this item covered or excluded under my policy?”

- “What is the next step after your visit?”

The adjuster may not give you a dollar amount on the spot. That is normal. They will file a report, and your insurer will send you a formal statement of loss.

Step 6: Get Your Own Repair Estimates

Do not rely solely on the adjuster’s estimate. Hire two or three local, licensed contractors to provide written estimates for the same scope of work. Ask them to break down:

- Water extraction and drying

- Demolition and debris removal

- Repairs to structural elements (covered)

- Replacement of covered items (furnace, water heater, sump pump)

- Mold prevention and treatment

These estimates serve two purposes. First, they help you understand the real cost of recovery. Second, they give you leverage if the insurance company’s offer seems too low.

Step 7: Review the Settlement Offer

Your insurer will send a document called a “proof of loss” or a settlement statement. For flood claims specifically (NFIP), you typically have 60 days to file a formal proof of loss. Read every line.

What you are looking for:

- Does the offer match your policy’s coverage limits?

- Are all covered items listed?

- Are the depreciation amounts reasonable? (actual cash value vs. replacement cost)

- Does the offer include your mitigation costs (pumps, fans, etc.)?

If the offer seems low, you have options. You can submit your contractor estimates and ask for a reconsideration. You can hire a public adjuster (more on this below). You can file an appeal. But first, call your adjuster and have an honest conversation. Many disagreements come from missing information, not bad faith.

Step 8: Complete Repairs and Submit Final Documentation

Once you accept the offer, the insurer will release payment. For mortgage holders, the check may be made out to both you and your lender. You will need your lender’s endorsement to cash it.

Hire your chosen contractor. Keep all receipts. When repairs are complete, submit any remaining invoices if you have a “replacement cost” policy that requires you to complete repairs before receiving the full payout.

Common Reasons Basement Flood Insurance Claims Get Denied

Denials happen. They are frustrating but often avoidable. Here are the most common reasons claims fail and how to prevent them.

Denial 1: “The water came from outside, and you do not have flood insurance.”

This is the most frequent denial by a wide margin. Homeowners assume “flood” means a river overflowing, not heavy rain seeping through basement walls. But insurance uses a stricter definition.

Prevention: Read your policy’s “water damage exclusion” section today. If it excludes “surface water,” “groundwater,” or “flood,” you need separate flood insurance.

Denial 2: “You did not maintain your property.”

Insurance covers sudden and accidental damage. It does not cover neglect. If your gutters have been clogged for five years and water poured down your foundation, that is maintenance, not a covered claim. If your sump pump was clearly broken for months, same issue.

Prevention: Keep records of gutter cleanings, downspout extensions, sump pump tests, and foundation seal inspections. Take photos each time. That proof matters during a claim.

Denial 3: “You waited too long to report or mitigate.”

Most policies require you to report a loss “promptly.” If you wait two weeks to file a basement flood insurance claim because you hoped the water would go away on its own, the insurer may argue that delays caused additional mold or structural damage.

Prevention: Report within 24 to 48 hours. Start mitigation the same day. Document your timeline with timestamps on photos.

Denial 4: “The item was not permanently installed.”

Remember the NFIP basement exclusion list. If you try to claim your basement sofa, your area rug, or your flat-screen TV, the adjuster will deny that line item immediately. This is not the insurer being unfair. This is the policy working exactly as written.

Prevention: Move valuable belongings out of your basement before flood season. Store them on upper floors or in waterproof containers elevated on blocks.

How to Maximize Your Payout (Ethically)

There is a difference between honest maximization and fraud. Fraud gets you canceled or prosecuted. These strategies are ethical, legal, and smart.

Strategy 1: Understand Actual Cash Value vs. Replacement Cost

Most flood policies pay actual cash value (ACV). That means replacement cost minus depreciation. A ten-year-old furnace might cost 5,000toreplace,butitsACVmightbe500.

Some private flood insurers offer replacement cost value (RCV) for an extra premium. RCV pays what it actually costs to buy a new item today.

Action step: Check your declarations page. If you have ACV, your settlement will reflect age and wear. That is normal. Do not expect new-for-old on a twenty-year-old water heater.

Strategy 2: Document Condition Before the Flood

Insurers depreciate based on remaining useful life. A three-year-old carpet has more value than a fifteen-year-old carpet. But you need to prove that carpet was in good shape.

Action step: Every year, walk through your basement with your phone. Open drawers. Show the furnace filter. Show the sump pump pit. Show the condition of your finishes. Store these videos in the cloud. This simple habit adds hundreds or thousands to a future claim.

Strategy 3: Hire a Public Adjuster for Large Losses

A public adjuster works for you, not the insurance company. They charge a fee (typically 5% to 15% of your settlement) but often secure much larger payouts. For losses under 10,000,hiringonerarelymakessense.Forlossesover30,000, their expertise can pay for itself.

Action step: If your basement flood damage exceeds $25,000, interview two or three licensed public adjusters. Ask for recent client references from similar basement flood claims.

Strategy 4: Appeal Depreciation

If the adjuster assigns excessive depreciation, you can push back. Provide receipts showing recent upgrades. Provide photos showing excellent condition. Provide contractor letters stating the item had substantial remaining life.

Action step: Write a clear, polite email to your adjuster. Attach your evidence. Say: “I respect your depreciation estimate on the furnace, but please see the attached receipt showing I replaced the motor eighteen months ago. That motor should not be fully depreciated.”

When to Hire a Lawyer for a Basement Flood Insurance Claim

Most claims do not need a lawyer. But some situations demand legal help.

Consider hiring an attorney if:

- Your claim is denied for reasons you believe are incorrect or in bad faith.

- Your settlement is more than $50,000 and the insurer refuses to negotiate.

- You have already filed an appeal and lost.

- Your policy contains confusing or contradictory language about basements.

Insurance bad faith is real. Insurers have a legal duty to handle claims fairly. If they unreasonably delay, deny without investigation, or misrepresent your policy, you may have a case.

Do not hire a lawyer for:

- Small claims under $10,000 (legal fees eat up the settlement).

- Denials clearly explained by your policy exclusions.

- Your first disagreement with the adjuster (try talking first).

Look for attorneys who specialize in property insurance or flood claims. Many offer free consultations. Ask about their experience with basement flood insurance claim cases specifically. Basements have unique rules, and a general lawyer may miss them.

Realistic Payout Examples (So You Know What to Expect)

Let us walk through three realistic scenarios. These numbers are based on average NFIP claims and actual homeowner experiences.

Scenario 1: Minimal Flood — Finished Basement with Old Items

- Cause: Heavy rain pushed water through a crack in the foundation wall.

- Water depth: 2 inches across 500 sq ft.

- Damage: Wet carpet padding, soaked boxes of holiday decorations, water line on drywall.

| Item | Covered? | Typical Payout |

|---|---|---|

| Carpet (10 years old) | No (finishing) | $0 |

| Drywall (painted) | No (finishing) | $0 |

| Cardboard boxes | No (personal property) | $0 |

| Furnace (no damage) | N/A | $0 |

| Sump pump (ran fine) | N/A | $0 |

| Water extraction (DIY) | Yes (mitigation) | $50 (for pump rental) |

| Total payout | $50 |

Result: The homeowner receives almost nothing. This is a hard truth. Many finished basement flood events are not worth filing a claim for after you consider deductibles and future premium increases.

Scenario 2: Moderate Flood — Unfinished Basement with Essential Equipment

- Cause: Sewer backup (with $10,000 rider on homeowners policy).

- Water depth: 6 inches across full basement.

- Damage: Destroyed furnace, water heater, sump pump, and electrical subpanel. Sewage contamination requires professional cleanup.

| Item | Covered? | Typical Payout |

|---|---|---|

| Furnace (5 years old) | Yes (ACV) | $3,500 |

| Water heater (3 years old) | Yes (ACV) | $900 |

| Sump pump (new) | Yes (ACV) | $250 |

| Electrical subpanel | Yes (RCV under rider) | $1,800 |

| Professional sewage cleanup | Yes (mitigation) | $2,000 |

| Less deductible | ($500) | |

| Total payout | $7,950 |

Result: The homeowner covers most major repairs. They pay out of pocket for drywall and paint if they choose to finish the basement again.

Scenario 3: Major Flood — Unfinished Basement with High-Value Mechanicals

- Cause: River overflow, NFIP flood policy with maximum $30,000 basement coverage.

- Water depth: 3 feet.

- Damage: Complete loss of furnace, water heater, boiler, two sump pumps, well pump, central AC compressor (basement unit), all electrical panels, fuel tank.

| Item | Covered? | Typical Payout |

|---|---|---|

| Furnace + boiler | Yes (ACV) | $6,000 |

| Water heater | Yes (ACV) | $800 |

| Two sump pumps | Yes (ACV) | $500 |

| Well pump | Yes (ACV) | $1,200 |

| AC compressor unit | Yes (ACV) | $2,500 |

| Electrical panels | Yes (ACV) | $3,000 |

| Fuel tank | Yes (ACV) | $1,200 |

| Cleanup and drying | Yes (mitigation) | $1,500 |

| Total payout | $16,700 |

Result: The homeowner receives a substantial check but must supplement with their own savings or a contractor payment plan. They do not receive coverage for their lost freezer full of meat, their washer/dryer, or their stored furniture.

Preventing Your Next Basement Flood (Cheaper Than a Claim)

The best basement flood insurance claim is the one you never file. Prevention is almost always more cost-effective than recovery.

Low-Cost Prevention (0–200)

- Clean gutters and downspouts twice a year. Extend downspouts at least five feet from your foundation.

- Grade soil away from your house. The ground should slope down one inch per foot for the first six feet around your foundation.

- Install window well covers. Clear plastic covers stop rain from filling window wells and seeping through basement windows.

- Test your sump pump monthly. Pour a bucket of water into the pit. The pump should turn on and empty it quickly.

Medium-Cost Prevention (200–2,000)

- Install a battery backup sump pump. When power fails, this keeps pumping. Cost: 300–600.

- Add a water alarm. A $20 device screams when water touches it. Place it near your sump pit, water heater, and floor drain.

- Seal foundation cracks. Hydraulic cement or epoxy injection costs 200–800 professionally. It stops small seepage before it becomes a flood.

- Install backwater valves. These prevent sewer backup by automatically closing when the city main backs up. Cost: 500–1,500 with installation.

High-Cost Prevention ($2,000+)

- Install a perimeter drain system (French drain). This collects water before it reaches your walls and channels it to your sump pit. Cost: 3,000–10,000.

- Waterproof basement walls from the exterior. Full excavation, sealing, and drainage. Cost: 10,000–30,000. Effective but expensive.

- Replace old cast iron sewer lines. Old lines crack and allow roots and water in. Cost: 5,000–15,000 depending on depth and access.

Return on prevention: A 500batterybackupsumppumpcanpreventa15,000 finished basement flood. That is a 30x return on investment. Prioritize medium-cost prevention before you need to file a basement flood insurance claim.

What About FEMA Assistance?

Many homeowners ask: “If a big storm floods my basement, will FEMA help?” The answer is complicated.

FEMA provides assistance only when the President declares a major disaster. That happens for significant, widespread events. Even then, FEMA assistance for basements is extremely limited.

FEMA Individual Assistance (for homeowners) typically covers:

- Temporary housing if your home is uninhabitable

- Essential home repairs (roof, walls, foundation to make it safe and sanitary)

- Replacement of essential personal property (bed, refrigerator, stove)

FEMA does NOT cover:

- Finished basement improvements (carpet, drywall, ceilings)

- Non-essential belongings (entertainment centers, exercise equipment, hobby items)

- Second refrigerators or freezers (unless the primary kitchen fridge was also damaged)

Important: FEMA assistance is not insurance. It is disaster relief. The maximum grant is typically around 40,000,butactualpayoutsaverage3,000 to $5,000. Unlike insurance, you cannot appeal a FEMA decision to get more. And you cannot receive FEMA assistance if you have flood insurance.

If you carry flood insurance, FEMA will tell you to file a basement flood insurance claim first. Only uninsured losses below your policy deductible or beyond your policy limits may qualify for supplemental FEMA aid.

The Emotional Side of Basement Floods

Let us be real for a moment. Insurance guides often sound robotic. But losing part of your home to water hurts. Maybe you stored your grandmother’s cedar chest down there. Maybe your kids’ artwork was in those boxes. Maybe you spent every weekend for a year building that home theater.

The insurance process will not fix those emotional losses. No check replaces sentimental value.

Give yourself permission to be frustrated. To cry if you need to. To feel angry at the rain, the city sewer department, or the insurance company. Those feelings are normal.

Then take a breath. Handle one task at a time. Document. Call. Mitigate. Wait. Repeat.

You are not alone. Millions of basements flood every year. Most homeowners eventually dry out, rebuild, and move forward. You will too.

And if the process feels overwhelming, ask for help. Friends can carry wet boxes. Your local emergency management office may have resources. The insurance company has a 24-hour claim line. There is no prize for suffering in silence.

Conclusion

Filing a basement flood insurance claim requires patience, documentation, and a clear understanding of what your policy actually covers. Most basements have limited protection, especially for finished spaces and personal belongings. By following the steps in this guide—stopping the water, documenting damage, filing promptly, meeting with the adjuster, and appealing when necessary—you give yourself the best chance of a fair settlement. Prevention remains your strongest tool, so invest in a battery backup sump pump and clean your gutters before the next storm arrives.

Frequently Asked Questions (FAQ)

1. Will my homeowners insurance cover a basement flood from heavy rain?

No. Standard homeowners insurance excludes flooding from rain, groundwater, and rising rivers. You need a separate flood insurance policy (NFIP or private) for those events.

2. How long do I have to file a basement flood insurance claim?

Most policies require you to report a loss “promptly.” For NFIP flood policies, you typically have 60 days to file a formal proof of loss. Report the claim within 24 to 48 hours to avoid denial for delay.

3. Does flood insurance cover finished basement floors and walls?

Under NFIP policies, no. Finished flooring, drywall, paneling, and paint are not covered in basements. Some private flood insurers offer broader coverage, but you must read your specific policy.

4. What if my sump pump fails during a storm?

Sump pump failure is only covered if you purchased a specific endorsement or rider on your homeowners policy. Without it, the damage is typically not covered. A battery backup pump prevents this situation.

5. Can I clean up before the adjuster arrives?

You can remove standing water and start drying the area to prevent further damage. But do not throw away damaged items, remove drywall, or make permanent repairs until the adjuster has inspected.

6. How much will my insurance premium increase after a flood claim?

It depends on your insurer, your claims history, and your location. One small claim under 5,000maynotraiseratessignificantly.Alarge30,000 claim likely will. For flood insurance through NFIP, your premium may increase if you file two or more claims within ten years.

7. What is a public adjuster, and should I hire one?

A public adjuster works for you, not the insurance company. They handle your claim for a percentage of the settlement (5–15%). For losses under 15,000,hiringonerarelymakesfinancialsense.Forlossesover30,000, their expertise often increases your payout enough to cover their fee.

8. Is mold damage covered after a basement flood?

Mold is covered only if it results from a covered water event and you took reasonable steps to dry the area quickly. If you ignored the water for two weeks, mold exclusion applies. Many policies have a specific mold sublimit (often 5,000to10,000).

Additional Resource

Link: Ready.gov/floods – Official FEMA flood preparedness guide. Includes downloadable checklists, flood map resources, and step-by-step instructions for before, during, and after a flood. Free and available in multiple languages.