For anyone running a boarding stable, the well-being of the horses in your care is your top priority. Right alongside that priority is the financial security of your business. That’s where horse boarding insurance comes in. It’s the essential safety net that protects you from devastating financial loss. But when you start looking into policies, one question inevitably rises to the top: what does horse boarding insurance cost?

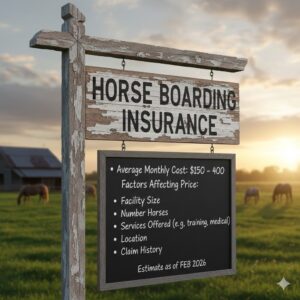

The answer, much like horses themselves, isn’t one-size-fits-all. The annual premium for a boarding stable can range significantly, from around $2,500 to over $10,000. This wide range exists because your cost is a direct reflection of your operation’s unique profile and risks.

In this comprehensive guide, we’ll move beyond ballpark figures. We’ll dissect the factors that insurers evaluate, explore the different types of coverage, and provide you with the knowledge to make an informed, confident decision for your stable’s future.

Horse Boarding Insurance Cost

What is Horse Boarding Insurance?

At its core, horse boarding insurance is a specialized package of liability and property coverages designed for businesses that house, care for, and train horses owned by others. It’s fundamentally different from personal horse owner insurance.

Think of it this way: if a horse owner’s policy covers their animal for mortality or medical expenses, the boarding insurance covers your liability as the business owner. Its primary purpose is to shield your assets—your property, your savings, your business itself—from claims arising from accidents, injuries, or damage that occur on your premises or due to your operations.

“A robust boarding insurance policy isn’t an expense; it’s an investment in the longevity of your business,” notes Sarah Jennings, a veteran equine insurance underwriter. “It’s what allows you to operate with peace of mind, knowing you have a partner in risk management.”

Key Factors That Determine Your Premium

Your insurance cost is calculated based on risk assessment. Insurers will look closely at the following aspects of your operation to determine how likely a claim is to occur.

1. Location and Property Details

-

Geography: Rates can vary by state and even region due to local litigation trends, weather-related risks (like hurricanes or wildfires), and veterinary care costs.

-

Facility Condition & Safety: Well-maintained fences, secure footing in arenas, clean barns with fire safety systems (smoke detectors, fire extinguishers), and good lighting all signal a lower-risk operation and can positively influence your cost.

-

Acreage & Number of Stalls: More land and more stalls generally mean higher liability exposure and potentially higher property values to insure.

2. Scope of Services & Activities

This is a major cost driver. Insurers categorize risk levels:

-

Full Care Boarding (Lowest Risk): Providing basic shelter, feed, and turnout.

-

Training: Adding professional training services increases risk.

-

Breeding Stallions/Mares: Introduces significant liability and care-specific risks.

-

Lesson Programs: Involving novice riders dramatically increases liability exposure.

-

Hosting Shows/Clinics: Temporary events add layers of public liability and participant risk.

-

Trail Riding Access: Allowing boarders to ride on your or adjacent property adds another dimension of risk.

3. Number of Horses Boarded

More horses directly correlate to higher liability. Your premium will be partly based on the average or maximum number of horses on the property.

4. Your Experience & Claims History

A stable owner with 20 years of experience and a clean claims history will typically receive more favorable rates than a new operation. A history of past claims will likely increase your premium.

5. Coverage Limits and Deductibles You Choose

You directly control these two levers:

-

Higher Liability Limits (e.g., $1 million vs. $500,000) = Higher Premium.

-

Higher Deductibles (the amount you pay out-of-pocket on a claim) = Lower Premium.

Comparative Cost Factors Table

| Factor | Lower Cost Scenario | Higher Cost Scenario |

|---|---|---|

| Services | Basic full-care boarding only | Training, lessons, breeding, hosted events |

| Facility | New fencing, modern barn, fire system | Older, worn fencing, outdated structures |

| Location | Low-population, low-litigation area | High-population state with frequent lawsuits |

| History | 10+ years in business, no claims | New business or multiple past claims |

| Coverage | $500,000 liability, $2,000 deductible | $2,000,000 liability, $500 deductible |

Breakdown of Core Coverage Types & Their Cost Impact

A typical boarding insurance package, often called a “Care, Custody, and Control” (CCC) policy, includes several components. Understanding each helps you see where your premium goes.

Care, Custody, and Control Liability (CCC)

-

What it is: The most critical part of boarding insurance. It covers your legal liability if a horse in your care is injured, becomes ill, or dies due to your alleged negligence.

-

Cost Impact: The base of your policy. Limits typically start at $500,000 and can go into the millions. Each increase in limit raises the premium.

General Liability (GL)

-

What it is: Covers third-party bodily injury (e.g., a visitor is kicked) or property damage (e.g., a boarder’s trailer is damaged on your property).

-

Cost Impact: Usually bundled with CCC. Essential and non-negotiable.

Property Coverage

-

What it is: Protects your physical assets—barns, tack rooms, arenas, fencing, and sometimes your business equipment.

-

Cost Impact: Directly tied to the replacement value of your insured structures. More/bigger buildings mean higher cost.

Equine Mortality & Major Medical (Optional but Critical)

-

What it is: While CCC covers your liability for a horse’s death, this optional coverage can be purchased to pay for the horse’s actual value (mortality) or surgical/medical costs (major medical) if it is injured or becomes ill, regardless of fault. This is often offered to boarders as an additional service.

-

Cost Impact: Adds significant premium but is a major value-add for clients. Cost is based on the horse’s value and medical limit chosen.

Helpful Lists for Boarding Stable Owners

Steps to Lower Your Insurance Premiums:

-

Increase Deductibles: Opt for a higher deductible you can comfortably afford.

-

Invest in Safety: Install fire alarms, post clear rules, maintain fencing, and document all safety inspections.

-

Use Ironclad Contracts: Have a lawyer-drafted boarding contract that includes liability waivers and clear rules. Provide this to your insurer.

-

Bundle Policies: Get your commercial auto, property, and liability from one provider.

-

Ask About Discounts: For paid-in-full annual premiums, for being claim-free, or for having certified safety training.

-

Regularly Review Horse Count: Report accurate average numbers to avoid over-insuring.

What to Look for in an Insurance Provider:

-

Specialization in equine or livestock insurance.

-

Financial strength and stability (check A.M. Best ratings).

-

Clear policy language and responsive customer service.

-

Access to risk management resources and advice.

-

A straightforward claims process with a dedicated adjuster.

Important Note for Readers

Never operate without insurance. A single lawsuit from an injured client or the loss of a valuable horse could result in a judgment that costs you your business, your property, and your personal assets. General farm insurance or a personal homeowner’s policy almost always excludes commercial boarding activities. You need a specific, commercial equine liability policy.

How to Get an Accurate Quote: A Practical Guide

Getting a quote isn’t just about a final number—it’s a process of discovery.

-

Gather Documentation: Have a summary of your services, number of stalls/acreage, photos of facilities, a copy of your boarding contract, and any safety manuals ready.

-

Choose Specialized Agents: Seek out 2-3 independent agents who work with multiple A-rated equine insurance carriers. Avoid agents who only offer one company’s products.

-

Be Thorough & Honest: Disclose all activities. Withholding information about lessons or events can void your policy when you need it most.

-

Compare Apples to Apples: Ensure each quote has the same liability limits, deductibles, and coverage inclusions. The cheapest quote may have dangerous exclusions.

-

Ask Questions: What’s excluded? How are claims handled? Is there a 24/7 emergency line? What risk management support do you offer?

Conclusion

Understanding horse boarding insurance cost requires looking beyond the premium to the unique variables of your stable. By investing in safety, choosing coverage wisely, and partnering with a specialized insurer, you secure not just a policy, but the future of your equine business. Protect your passion with the right foundation.

Frequently Asked Questions (FAQ)

Q: What is the single biggest factor affecting my cost?

A: The scope of your services. Adding lessons, training, or public events introduces significantly more risk than basic boarding and will increase your premium more than any other single factor.

Q: Can I require my boarders to have their own insurance?

A: Absolutely, and you should. Include a clause in your contract requiring boarders to carry their own mortality and major medical insurance. This protects the horse owner and can help prevent disputes. However, their policy does not replace your commercial liability insurance—it complements it.

Q: Are there any coverage exclusions I should watch out for?

A: Always read the exclusions. Common ones can include injuries from certain high-risk activities (e.g., racing, breeding stallions if not declared), transportation of horses (may require a separate endorsement), and deliberate acts of negligence. Full disclosure to your agent is key to avoiding coverage gaps.

Q: How often should I review my policy?

A: At least annually, or whenever you make a significant change to your operations (adding a new arena, starting a lesson program, increasing your horse capacity).