If you work in healthcare, law, finance, or any profession where clients rely on your advice, you already know that mistakes happen. Even when you do everything right, someone might claim you made an error. That is why you need malpractice insurance.

But here is where many professionals get stuck. You go to buy a policy, and the agent asks you a question that sounds simple: “Do you want occurrence or claims-made coverage?”

Suddenly, you feel lost. You are not alone.

Understanding the difference between occurrence and claims made malpractice insurance can save you thousands of dollars. More importantly, it can prevent a nightmare scenario where you think you are covered, but your insurance company refuses to pay.

This guide will walk you through everything you need to know. No confusing legal terms. No hidden tricks. Just honest, practical information to help you make the right choice.

What Is Malpractice Insurance? A Quick Refresher

Before we dive into the differences, let us make sure we are on the same page about what malpractice insurance actually does.

Malpractice insurance is a type of professional liability insurance. It protects you when a client or patient says you made a mistake that caused them harm. That harm could be physical, financial, or emotional.

For example, a doctor might miss a diagnosis. A lawyer might file a document after the deadline. An accountant might make a math error on a tax return. In all these cases, the professional could face a lawsuit.

The insurance policy pays for:

- Legal defense costs (lawyers, court fees, expert witnesses)

- Settlements or judgments against you

- Court costs and administrative expenses

Without this coverage, you would have to pay these costs out of your own pocket. A single lawsuit can easily cost over $100,000 to defend, even if you win. If you lose, the judgment could be millions.

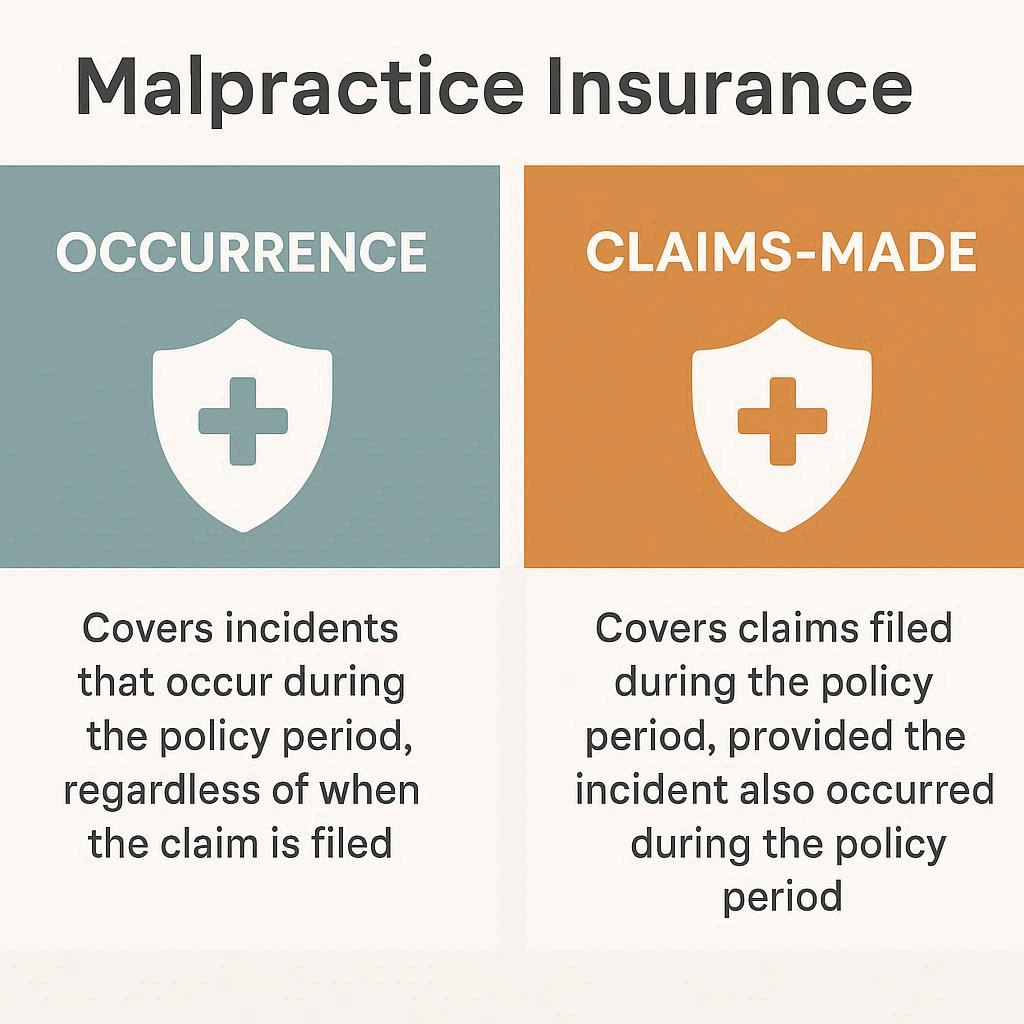

Now, here is where things get tricky. Not all malpractice policies work the same way. The timing of when a claim must be reported is the key difference between the two main types.

The Core Difference: It Is All About Timing

Let me give you the straight answer right now. The difference between occurrence and claims made malpractice insurance comes down to one simple question: When must you report a claim?

| Feature | Occurrence Policy | Claims-Made Policy |

|---|---|---|

| When does coverage apply? | When the incident happened | When the claim is reported |

| Do you need to report claims after the policy ends? | No, you are still covered | Yes, unless you buy tail coverage |

| Typical cost at the start | Higher | Lower |

| Long-term cost | Stable | Increases over time |

| Best for | Lifetime protection, retirement | Short-term or budget-conscious needs |

How an Occurrence Policy Works

Imagine you buy an occurrence policy that is active from January 1, 2020, to January 1, 2021. During that year, you treat a patient or advise a client. Then, on January 1, 2021, you cancel the policy because you retire.

Now, fast forward three years. It is 2024. That patient from 2020 decides to sue you for something that happened during your treatment. You have not had an active policy for three years.

Are you covered?

With an occurrence policy, yes, you are covered. The policy was active when the incident occurred. That means the policy is responsible for that incident, even if the lawsuit comes years later. The insurance company cannot say, “Sorry, your policy ended.”

This is why many professionals love occurrence policies. They offer peace of mind. Once you have coverage for a period of time, those years are protected forever.

How a Claims-Made Policy Works

Now, let us look at the same scenario with a claims-made policy.

You buy a claims-made policy from January 1, 2020, to January 1, 2021. You treat a patient in 2020. You cancel the policy on January 1, 2021. In 2024, the patient sues you.

With a claims-made policy, the answer is different. You are not covered. Why? Because the claim was reported in 2024, and you did not have an active claims-made policy in 2024. The policy only covers claims that you report while the policy is active.

This sounds scary, right? But there is a solution. That solution is called “tail coverage,” and we will talk about that in detail later.

Important Note: Claims-made policies only cover claims that are both:

- Caused by an incident that happened on or after the policy’s retroactive date

- Reported to the insurance company while the policy is active

Breaking Down Occurrence Policies: The Deep Dive

Now that you understand the basic difference, let us look at each type in detail. We will start with occurrence policies because they are simpler to understand.

What Does an Occurrence Policy Actually Cover?

An occurrence policy covers any incident that takes place during your policy period, regardless of when someone files the claim. The “trigger” for coverage is the date of the incident, not the date of the claim.

Here is a real-world example.

Dr. Sarah is a pediatrician. She has an occurrence policy from ABC Insurance from January 1, 2023, to January 1, 2024. On June 15, 2023, she sees a young patient named Leo. Leo has a fever and a cough. Dr. Sarah diagnoses a common virus and sends Leo home.

Two years later, Leo is diagnosed with a more serious condition. The parents believe Dr. Sarah should have caught it earlier. They file a lawsuit on March 10, 2025.

Dr. Sarah stopped practicing medicine in December 2024. She let her occurrence policy expire because she retired. But guess what? The lawsuit from 2025 is still covered. The incident happened on June 15, 2023, when Dr. Sarah’s occurrence policy was active. The insurance company must defend her and pay any settlement or judgment.

The Pros of Occurrence Policies

Many professionals prefer occurrence policies for good reasons.

Lifetime protection. Once you have coverage for a specific year, that year is protected forever. You do not need to keep paying premiums to stay protected for past work.

No tail coverage needed. When you leave a job or retire, you do not need to buy an expensive tail policy. You can simply walk away knowing your past work is still covered.

Predictable and simple. You never have to worry about whether a claim was reported on time. The only question is, “Did the incident happen while I had coverage?”

Great for retirement planning. Many professionals work for decades and then retire. An occurrence policy makes retirement cleaner. You do not have to keep paying insurance forever.

The Cons of Occurrence Policies

No insurance product is perfect. Occurrence policies have some drawbacks.

Higher upfront cost. Insurance companies know they are taking on more risk. They might have to pay a claim 10 or 20 years from now. That is a long time to keep money reserved. So they charge higher premiums at the start.

Not all carriers offer them. In some professions, occurrence policies are becoming rarer. Many insurance companies have switched to claims-made only.

Inflation risk for insurers. A claim filed 15 years later might cost much more to settle than it would have at the time. Insurance companies account for this in your premium, which makes the policy more expensive.

Who Should Choose an Occurrence Policy?

You are a good candidate for an occurrence policy if:

- You plan to work for many years and then retire completely

- You want the simplest, most predictable coverage

- You have the budget for higher upfront premiums

- You hate paperwork and do not want to track reporting deadlines

- You are in a high-risk specialty where lawsuits often come years later (like obstetrics or surgery)

Breaking Down Claims-Made Policies: The Deep Dive

Claims-made policies work differently. They are more common today, especially in medicine and law. Let us understand why.

What Does a Claims-Made Policy Actually Cover?

A claims-made policy covers claims that meet two conditions:

- The incident happened on or after your policy’s “retroactive date”

- You report the claim to the insurance company while the policy is active

Let me explain the retroactive date. When you first buy a claims-made policy, the insurance company sets a retroactive date. That date is usually the same as your policy start date. This means the policy only covers incidents that happen after you bought the policy.

However, if you stay with the same insurance company for many years, the retroactive date stays the same. So after five years, your retroactive date might be five years ago. That means the policy covers incidents from the last five years, as long as you report claims while the policy is active.

Here is an example to make this clear.

Dr. James buys his first claims-made policy on January 1, 2019. His retroactive date is January 1, 2019. He sees a patient on March 10, 2019. On December 15, 2019, the patient files a claim. Dr. James reports it immediately. Covered. Both conditions are met: the incident happened after the retroactive date, and he reported it while the policy was active.

Now, Dr. James renews his policy every year. By 2024, his retroactive date is still January 1, 2019. A patient he saw in 2020 files a claim in 2024. He reports it while his 2024 policy is active. Covered.

But here is the catch. If Dr. James cancels his policy in 2024 and does not buy tail coverage, a claim filed in 2025 for an incident in 2020 would not be covered.

The Pros of Claims-Made Policies

Claims-made policies are popular for several reasons.

Lower initial premiums. In the first year, a claims-made policy costs much less than an occurrence policy. This helps new professionals who are just starting their careers.

Gradual premium increases. As you stay with the same carrier, your premium goes up each year. But it increases slowly. By year five or six, the premium might be similar to an occurrence policy.

Easier to find. Many insurance companies have stopped selling occurrence policies. Claims-made is the standard in many fields. You may not have a choice.

Better for short-term work. If you only plan to work for a few years, a claims-made policy can save you money. You just need to handle the tail coverage when you stop.

The Cons of Claims-Made Policies

The drawbacks of claims-made policies can be serious if you are not careful.

You need tail coverage when you leave. This is the biggest downside. When you cancel a claims-made policy, you have a problem. Any future claims from past work will not be covered. The only solution is to buy “tail coverage” (also called an extended reporting period or ERP). Tail coverage can cost 150% to 300% of your last annual premium.

You must report claims quickly. If a patient threatens to sue, you need to report it to your insurance company immediately. If you wait until after your policy ends, you might lose coverage.

Switching carriers is complicated. If you want to switch from one claims-made carrier to another, the new carrier might not give you full retroactive coverage. You may need to buy tail from the old carrier and nose coverage from the new carrier. This gets expensive and messy.

Long-term cost can be higher. While early years are cheap, the total cost over 20 or 30 years can exceed the cost of an occurrence policy, especially when you add tail coverage at the end.

Who Should Choose a Claims-Made Policy?

A claims-made policy might be right for you if:

- You are just starting your career and have a tight budget

- You work for an employer who provides claims-made coverage (many hospitals do this)

- You only plan to work for a few years

- You understand tail coverage and have a plan for it

- Occurrence policies are not available in your field

Tail Coverage: The Most Important Thing You Need to Understand

If you have a claims-made policy, tail coverage is not optional. It is essential. Let me explain why.

What Is Tail Coverage?

Tail coverage is an endorsement you buy when you cancel a claims-made policy. It gives you time to report claims after the policy ends. Usually, tail coverage lasts forever. Once you buy it, you can report any claim from past incidents at any time in the future.

Think of it this way. Your claims-made policy is like a membership that only works while you are paying dues. When you stop paying, the membership ends. Tail coverage is like buying a lifetime membership for your past work.

How Much Does Tail Coverage Cost?

The honest answer is: it depends. But here are general ranges.

| Years with same carrier | Tail cost (% of last premium) |

|---|---|

| 1 year | 150% – 200% |

| 3-5 years | 200% – 250% |

| 5-10 years | 250% – 300% |

| 10+ years | 300% or more |

So if your last annual premium was $10,000, your tail coverage could cost $15,000 to $30,000 or more. That is a significant expense. Many professionals are shocked when they see this number for the first time.

Who Pays for Tail Coverage?

This depends on your situation.

If you are an employee: Some employers pay for tail coverage when you leave. This is common in hospitals and large group practices. Always check your employment contract. If it is not written down, do not assume they will pay.

If you are a partner in a group: Partnership agreements often spell out who pays for tail coverage. Many groups pay for tail coverage for retiring partners but not for partners who leave to join another practice.

If you are a solo practitioner: You pay for your own tail coverage. There is no one else to cover it.

If you are switching carriers: Your new carrier might offer “prior acts coverage” or “nose coverage.” If they do, you might not need to buy tail from the old carrier. But you must make sure there is no gap in coverage.

Nose Coverage: The Other Side of the Coin

Nose coverage is less common but important to understand. When you switch from one claims-made carrier to another, the new carrier might offer nose coverage. This means they agree to cover claims from incidents that happened before your new policy started, as long as you had continuous coverage.

Nose coverage is usually cheaper than tail coverage from your old carrier. But not all carriers offer it. And you need to buy it when you start the new policy, not later.

Real-World Scenarios: Which Policy Wins?

Let us look at five common situations. In each case, I will tell you which policy works better and why.

Scenario 1: The New Graduate

Maria just finished her medical residency. She is 29 years old. She plans to work for 35 years and then retire. She does not have much money right now.

Better choice: Claims-made. Maria can start with low premiums. As her income grows, her premiums will increase gradually. She can save money now when she needs it most. In 35 years, she will buy tail coverage when she retires. By then, she will have saved enough to afford it.

Scenario 2: The Solo Practitioner Approaching Retirement

Dr. Patel is 62 years old. He has run his own private practice for 30 years. He plans to retire in three years. He has an occurrence policy right now.

Better choice: Stay with occurrence. Dr. Patel already has occurrence coverage. He should keep it until retirement. When he retires, he can simply stop paying. No tail needed. If he switched to claims-made now, he would have to pay three years of premiums plus expensive tail coverage at the end. That does not make financial sense.

Scenario 3: The Hospital Employee

Lisa is a nurse anesthetist. She works for a large hospital system. The hospital provides her claims-made malpractice insurance. She plans to stay at this hospital for her whole career.

Better choice: Claims-made (employer-provided). Lisa does not pay for her own policy. The hospital covers the premiums and will likely pay for tail coverage when she retires or leaves. She should check her employment contract to confirm the tail coverage provision. If the hospital pays for tail, she has nothing to worry about.

Scenario 4: The Short-Term Contractor

John is a lawyer who takes six-month contracts. He works for one firm, then another. He never stays anywhere longer than a year.

Better choice: Occurrence (if available). John needs simplicity. If he buys claims-made policies for each short contract, he would need tail coverage after every single contract. That is expensive and annoying. An occurrence policy covers each contract period permanently. He pays more upfront but saves on tail costs.

Scenario 5: The High-Risk Specialist

Dr. Williams is an obstetrician. She delivers babies. Lawsuits in obstetrics can be filed years later when a child develops problems that might be linked to birth injuries.

Better choice: Occurrence. Because claims can come decades later, occurrence coverage is safer. With a claims-made policy, Dr. Williams would need to keep paying premiums or buy tail coverage for her entire career. Even after retirement, she might need coverage for decades. An occurrence policy eliminates this uncertainty.

Common Myths and Mistakes

Let me clear up some confusion I see all the time.

Myth 1: “Claims-made policies are cheaper overall”

This is not always true. Claims-made policies have lower initial premiums, but the total cost over a full career plus tail coverage can be higher than an occurrence policy. You need to do a long-term comparison, not just look at year one.

Myth 2: “I do not need tail coverage because I am retiring”

Wrong. If you have a claims-made policy, you absolutely need tail coverage when you retire. Without it, a lawsuit filed after retirement will not be covered. Imagine being sued at age 75 and having no insurance. That is a disaster.

Myth 3: “My new policy will cover past claims automatically”

Not necessarily. When you switch carriers, you must specifically negotiate prior acts coverage or nose coverage. Do not assume it is included. Always ask, “Does this policy cover claims from incidents that happened before the policy start date?”

Myth 4: “Occurrence policies never have problems”

Occurrence policies are great, but they are not magic. If you let your occurrence policy lapse and then have an incident during the lapse period, you are not covered. Also, occurrence policies can have limits that might be too low for claims filed many years later.

Mistake to Avoid: Changing policies without a plan

The biggest mistake I see is professionals switching from claims-made to occurrence (or vice versa) without understanding the consequences. If you switch from claims-made to occurrence, you still need tail coverage from your claims-made policy for the years before the switch. The new occurrence policy will not cover past incidents.

How to Choose the Right Policy for You

Making this decision does not have to be overwhelming. Follow these steps.

Step 1: Know your career timeline

Ask yourself honestly: How many more years will I work? Will I retire completely or work part-time? Do I plan to switch jobs often? Your answers will point you in the right direction.

| Career situation | Recommended policy |

|---|---|

| Long career, single employer, lifetime protection desired | Occurrence |

| Long career, budget is tight early on | Claims-made with a tail plan |

| Short career (under 5 years) | Claims-made with tail at the end |

| High risk of late claims (OB, surgery, law) | Occurrence |

| Employer provides coverage | Follow employer’s plan |

Step 2: Compare total lifetime costs

Do not just look at next year’s premium. Estimate your total cost over your entire career plus tail coverage (if needed). Ask insurance agents to give you a 10-year projection. Compare occurrence vs. claims-made over that full period.

Step 3: Check what is available in your state

Some states have regulations that favor one type of policy. In some medical fields, occurrence policies are no longer sold to new customers. Check with at least three insurance brokers to see what is actually available to you.

Step 4: Read your employment contract carefully

If you are an employee, your contract might require you to have a certain type of policy. It might also state whether your employer pays for tail coverage. Never assume. Always get it in writing.

Step 5: Ask these five questions before you buy

- “Is this policy occurrence or claims-made?”

- “If claims-made, what is the retroactive date?”

- “What is the cost of tail coverage if I leave or retire?”

- “Do you offer nose coverage if I switch carriers later?”

- “Has this carrier raised premiums significantly in the past five years?”

Important Notes for Readers

Note 1: Tail coverage must be purchased when you cancel your claims-made policy. You cannot buy it later. If you forget, you lose the right to buy it. Set a reminder well before your policy ends.

Note 2: Some claims-made policies include “free tail” after a certain number of years. For example, if you stay with the same carrier for 10 years, they might provide tail coverage at no additional cost when you retire at age 65 or older. Ask about this. It is rare, but some carriers offer it.

Note 3: If you die, your estate may still need tail coverage. Lawsuits can be filed against a deceased professional’s estate. Make sure your family knows about your insurance and any tail coverage obligations.

Note 4: Part-time work after retirement can complicate your coverage. If you retire but then do occasional consulting, you may need to keep some form of active coverage. Talk to your agent before reducing your hours.

Note 5: Do not cancel any malpractice policy until you have a new policy in place. Even a one-day gap can leave you exposed. Claims for incidents that happen during the gap will not be covered by your old policy or your new policy.

The Financial Reality: What You Will Actually Pay

Let me give you realistic numbers. These are estimates based on typical rates. Your actual premiums will vary based on your profession, specialty, location, claims history, and coverage limits.

Occurrence Policy Premiums (Annual)

| Profession | Year 1 | Year 5 | Year 10 | Year 20 |

|---|---|---|---|---|

| General physician | $8,000 | $8,500 | $9,500 | $11,000 |

| Surgeon | $25,000 | $27,000 | $30,000 | $35,000 |

| Lawyer (private practice) | $3,500 | $3,800 | $4,200 | $5,000 |

| Accountant | $1,500 | $1,600 | $1,800 | $2,200 |

Occurrence premiums start higher but increase slowly. They mostly go up due to inflation and general rate increases, not because of the policy structure.

Claims-Made Policy Premiums (Annual)

| Profession | Year 1 | Year 5 | Year 10 | Year 20 | Tail (after year 20) |

|---|---|---|---|---|---|

| General physician | $3,000 | $7,000 | $9,000 | $11,000 | $22,000 – $33,000 |

| Surgeon | $10,000 | $22,000 | $28,000 | $35,000 | $70,000 – $105,000 |

| Lawyer (private practice) | $1,200 | $2,800 | $3,800 | $5,000 | $10,000 – $15,000 |

| Accountant | $600 | $1,400 | $1,800 | $2,200 | $4,400 – $6,600 |

Notice how claims-made premiums start low but catch up to occurrence by year 10 or so. The tail cost at the end is a significant additional expense.

Important Note: Some claims-made policies have “step-rated” premiums. That means your premium increases on a fixed schedule for the first five years, regardless of claims. After year five, it becomes experience-rated (based on your actual claim history). Ask your agent if your policy is step-rated.

Switching Between Carriers: A Step-by-Step Guide

If you already have a claims-made policy and want to switch to another claims-made carrier, follow this process carefully.

Step 1: Do not cancel your old policy yet.

Step 2: Find a new carrier willing to give you “prior acts coverage” or “nose coverage.” This means they will cover claims from incidents that happened before your new policy started. You need continuous coverage with no gaps.

Step 3: Get written confirmation from the new carrier about the retroactive date they will offer. Ideally, they will match your old retroactive date. If they offer a later date, you have a gap in coverage.

Step 4: Once the new policy is active, you can cancel your old policy. You do not need tail coverage from the old carrier because the new carrier is covering your prior acts.

Step 5: Keep all your old policy documents forever. You may need them to prove continuous coverage.

If you want to switch from claims-made to occurrence, you need to buy tail coverage from your claims-made carrier. The new occurrence policy will only cover incidents that happen after it starts. It will not cover past incidents. So you must have tail for the claims-made years.

If you want to switch from occurrence to claims-made, you can do so easily. The claims-made policy will set its retroactive date to the start of your occurrence policy. This is one of the few simple transitions.

State Regulations and Special Situations

Malpractice insurance is regulated at the state level. Some states have unique rules.

California: The Medical Insurance Feasibility Commission (MIRC) provides tail coverage for physicians in certain situations. If your claims-made carrier becomes insolvent, MIRC may help. But do not rely on this. Buy your own tail coverage.

Florida: Florida law requires medical malpractice insurers to offer tail coverage when a claims-made policy ends. But you still have to pay for it. The insurer just has to make it available.

New York: New York has special rules for physicians who participate in the state’s medical malpractice insurance pool. Tail coverage rules differ for participants.

Texas: Texas has a patient compensation fund that can affect large judgments. This may influence your coverage limits but not the occurrence vs. claims-made decision.

What about telemedicine and multi-state practice?

If you practice across state lines, you need coverage that works in every state where you see patients. Some carriers offer “national” policies. Others limit you to specific states. The occurrence vs. claims-made decision does not change across states, but the availability of each type might.

What about part-time or moonlighting work?

If you work part-time for a different employer, check whether that employer’s policy covers you. Often, it does not. You may need your own separate policy. For occasional low-risk work, a claims-made policy with a high deductible might be affordable. For regular part-time work, an occurrence policy gives you simpler protection.

Additional Resource

For an independent comparison of malpractice insurance carriers and real customer reviews, visit the National Practitioner Data Bank (NPDB) guide page. While the NPDB itself does not endorse insurers, their public use data files show which carriers have the most reported claims. You can access this data at: https://www.npdb.hrsa.gov

Note: This link leads to a government resource for research purposes. Always verify any insurance decision with a licensed broker in your state.

Conclusion

Choosing between occurrence and claims-made malpractice insurance comes down to timing and your career plans. Occurrence policies cover incidents that happen during your policy period, no matter when the claim is filed. Claims-made policies only cover claims reported while the policy is active, which means you need tail coverage when you leave or retire. For most long-term professionals, occurrence offers simpler lifetime protection, while claims-made works well for short-term work or when budget is tight early in your career.

Frequently Asked Questions (FAQ)

Q1: Can I have both occurrence and claims-made policies at the same time?

Yes, but it is rarely necessary. Some professionals keep a small occurrence policy for tail purposes while using a claims-made policy for current work. Talk to an agent before doing this to avoid double-paying.

Q2: Does tail coverage ever expire?

Most tail coverage is “unlimited” or “perpetual.” Once you buy it, it lasts forever. But a few carriers offer limited tail coverage of 1, 3, or 5 years. Never buy limited tail coverage for a permanent retirement. Only buy unlimited tail.

Q3: What happens if my insurance company goes out of business?

If a claims-made carrier becomes insolvent, your tail coverage may be worthless. Occurrence policies are safer in this regard because the coverage is tied to the incident date, not the carrier’s future existence. Most states have guaranty funds that may help, but they have limits.

Q4: Can I negotiate tail coverage cost?

Sometimes. If you have been with the same carrier for many years without claims, you can ask for a discount on tail coverage. Some carriers will negotiate, especially if you are retiring completely. Always ask.

Q5: Do I need tail coverage if I am switching to an in-house position with an employer who provides coverage?

Yes, unless the employer agrees to cover your past acts. Most employer policies only cover work done for that employer. They do not cover your previous private practice work. You need tail coverage for your prior solo or group work.

Q6: How long do I have to report a claim under a claims-made policy?

Your policy will specify a reporting window, usually 30 to 60 days after the policy ends. But you should report potential claims immediately. Never wait. If you miss the window, you lose coverage entirely.

Q7: Is tail coverage tax-deductible?

Yes, in most cases. Tail coverage is considered a business expense. For self-employed professionals, it is fully deductible. For employees, it may be deductible as an unreimbursed business expense depending on tax laws. Consult your tax advisor.

Q8: What is the difference between tail coverage and nose coverage?

Tail coverage extends your old policy to report claims after it ends. Nose coverage is a feature of a new policy that covers past incidents. You buy tail from your old carrier. You look for nose coverage from your new carrier.

Q9: Do I need malpractice insurance if I work for a large hospital or corporation?

Yes, but possibly not your own policy. The hospital’s policy likely covers you for work done at the hospital. However, that policy may not cover you for moonlighting, consulting, or volunteer work. Always check the policy’s scope. Many employed professionals buy a separate, low-cost “supplemental” policy for outside activities.

Q10: Can I be sued after I die?

Yes. Your estate can be sued for malpractice claims that arose before your death. If you had a claims-made policy without tail coverage when you died, your estate has no protection. This is why estate planning should include a discussion of tail coverage.

Disclaimer: This article is for educational and informational purposes only. It does not constitute legal advice or insurance advice. Insurance laws, regulations, and policy terms vary significantly by state and profession. You should always consult with a qualified insurance broker or attorney who is familiar with your specific situation before purchasing or changing any malpractice insurance policy. The author and publisher disclaim any liability for any actions taken based on the information in this article.